GCC Supply Invoice -Excel and Word download

Introduction

The Member states of the Gulf Cooperation Council, namely (United Arab Emirates, Kingdom of Bahrain, Kingdom of Saudi Arabia, Sultanate of Oman, State of Qatar and State of Kuwait)have introduced VAT from January 2018.VAT is an indirect ConsumptionTax that must be charged by the businesses to their clients on the supply of goods and services at the rate of 5%.Companies in the GCC or doing business in the GCC are all governed by the VAT Rules.

Learning from the post

- What is GCC Supply?

- What are GCC transactions?

- What is place of supply?

- Conditions for raising GCC Supply Invoice

- Issuance of GCC Supply

- Contents of GCC Supply

- Retention period of Tax Invoices

- Download Invoice template Excel/Word

- How to raise a GCC Supply Invoice through Reach Online Accounting Software

What is GCC Supply?

A Taxable Person who transports Goods for the purposes of his business from the place where they are in a Member State to another place in another Member State shall be deemed to have made a Supply of Goods. When goods are transported from one GCC member state to another GCC member state, it is called GCC Supply.The place of supply depends on whether the customer is a VAT taxable person.

What are GCC Transactions?

Intra-GCC transactions are the transactions (sales and purchases) between member states of GCC. Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and UAE have signed the GCC VAT Agreement.

What is Place of Supply?

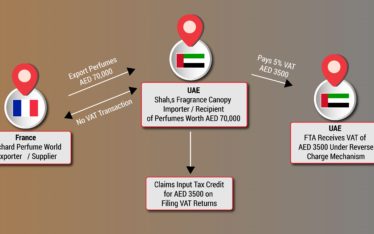

If the Taxable Person in a Member State receives taxable Goods or Services from a Person who is a resident in another Member State, then he shall be deemed to have supplied these Goods or Services to himself and the Supply shall be taxable in accordance with the Reverse Charge Mechanism.

If a Taxable Person residing in a Member State receives Services from a person who is not resident in the GCC Territory, then that Person shall be deemed to have supplied these Services to himself and the Supply shall be taxable according to the Reverse Charge Mechanism.

Examples:

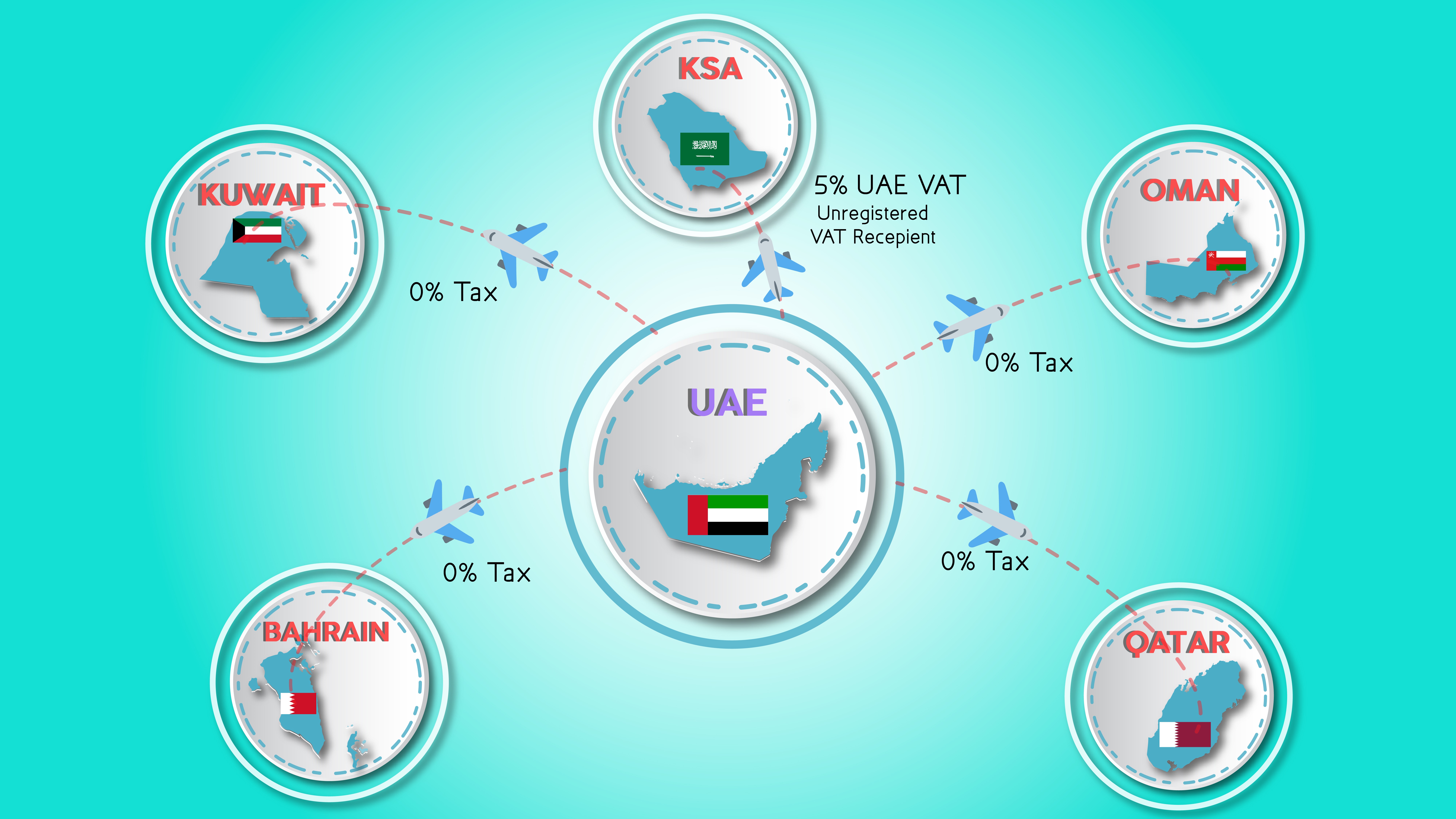

(i) If the customer is a VAT-registered taxable person, then the place of supply is the member state that is the goods’ final destination.

For example, if a supplier in UAE sells confectioneries to a VAT-registered customer in the KSA, the place of supply is the KSA. This also requires the customer to pay the VAT under the reverse-charge mechanism.

(ii) If the customer is not a VAT-registered taxable person, the place of supply depends on whether the supplier exceeds the VAT export threshold.

Conditions for raising GCC Supply Invoice

- The customer should be registered with VAT authorities in his state.

- If he is not registered he should be below the mandatory threshold.

- If any of these conditions are not met, then a normal Tax invoice should be raised and the supply will be taxable.

Below threshold Exceeding threshold

- The total amount of exports by the supplier is below the mandatory registration threshold in the destination member state.

- The total amount of exports by the supplier is above the mandatory registration threshold in the destination member state.

Place of supply is UAE, and UAE VAT should be paid. Place of supply is the destination member state, and VAT should be paid in that state.

Issuance of GCC Supply Invoice:

1 .The Taxable Person must issue a Tax Invoice in the following cases:

a) Supply of Goods or Services including a Deemed Supply

b) Full or partial receipt of Consideration prior to the supply date.

2. Each Member State may allow the Taxable Person to issue summary tax invoices, each including all the supplies of Goods and service made in favour of a single Customer that were taxable over a period of one month

3. The Member States must accept the invoices in form, whether issued on paper or electronically, in accordance with the conditions and procedures determined by each Member State.

Contents of GCC Supply Invoice:

1. Each Member State must determine the contents of the Tax Invoice and the period within which it must be issued, provided that The Ministerial Committee shall determine the minimum details required to be included in the tax invoice. Each Member State may allow for the issuance of simplified invoices in accordance with the conditions and rules determined by it.

2. Tax invoices can be issued in any currency, provided that the value of the Tax is written in the currency of the Member State where the place of supply is located based on the official currency exchange rate in force in that State as on the Tax due date.

Amendment of GCC Supply Invoices (Credit Notes)

A Taxable Person who adjusts the Supply Consideration must include this adjustment in a document (credit or debit note “Tax Invoice”) correcting the original Tax Invoice. This document shall be treated in the same way as the original Tax Invoice according to the procedures determined by each Member State.

Retention Period for Tax Invoices, Records and Accounting Documents

Without prejudice to any longer period stipulated under the laws of the Member State, Tax Invoices, books, records and accounting documents shall be retained for a period not less than five years from the end of the year to which the invoices, books, records and accounting documents relate. This period shall be extended to fifteen years for the retention of Tax Invoices, books, records and documents pertaining to real estate

GCC Supply Invoice Format – Excel and Word Download

Popular posts

Related Blogs