Import Of Services in UAE-Learn Online with Reach Accountant

Introduction

What does Import of Services in UAE mean?

When services are purchased from other countries for the beneficial use of UAE it means import of services in UAE. Most of the services in the UAE are imported from Europe and Asia, while a few come from other GCC countries.

What’s in the post?

- What does Import of Services in UAE mean?

- What should be treated as supply of services?

- Determining Place of supply for import of services

- Place of Supply Services – Reverse charge mechanism

- Imports from outside GCC

- B2B Import into UAE from outside of GCC

- General services from a supplier in KSA to a customer in UAE

- Example of Import Of Services ·

- VAT on E-Commerce

- Accounting Entry for Import Of Services in UAE

- Reach Accountant Online Video learning for Import of services in UAE

- Conclusion

VAT will apply on the supply of goods and services in the UAE (including imports) by a taxable person for consideration and during the course of business, except on the exempt goods and services as specified under the VAT Law.

What should be treated as supply of services for import of services in UAE

The UAE Executive Regulation has detailed few specific forms of supply which should be treated as a supply of services.

The following should be treated as a supply of services:

- The granting, assignment, cessation, or surrender of a right

- Making available a facility or advantage

- Not to participate in any activity, or not to allow its occurrence, or agree to perform any activity

- The transfer of an indivisible share in a good

- The transfer or licensing of intangible rights, for example, rights of authors, inventors, artists, and rights in trademarks.

The businesses who are in the Services sector need to take extra care in determining whether a supply is a service or goods. This is because, services are defined to include ‘non-physical’ property along with ‘anything’ else that can be supplied other than goods. Thus, it is capable of encompassing all transactions that escape the definition of goods into services.

Based on the GCC Agreement, use and enjoyment provisions should apply to electronically supplied services. It will be up to each GCC member state to define those services in more detail. The place of supply will be the GCC member state where the ESS is used and enjoyed. If the customer is a VAT registered taxable person, it may be able to self-account for the VAT due under the reverse-charge mechanism. However, if the customer is not VAT registered (e.g. an individual consumer), then the offshore provider will likely have to register for VAT in the GCC member state where the service is used and enjoyed, so it can charge VAT

Determining Place of supply for import of services in UAE

If the supply is treated as made in the UAE VAT may be charged.

- Place of supply of services supplied by a person that is not resident in the UAE to a VAT registered business resident in the UAE is in the UAE

- Place of supply of restaurant, hotel and catering services is where they are performed

- Place of supply of services supplied to recipients who are VAT registered in another GCC State is that other GCC State unless the place of supply is the UAE for another reason

- Place of supply of services relating to the installation of goods is where the service is performed

- Place of supply of real estate services is the location of the real estate

- Place of supply of transport services is where the transport begins

- Place of supply of cultural, artistic, sporting, educational or similar services is where they are performed

- Imports from outside GCC If the supplier is a non-UAE resident who provides service to a VAT-registered resident in the UAE, then the place of supply is the UAE

- The place of supply for wired and wireless telecommunication services and electronically supplied services will be the location where the services are used or received.

| S.No | Residence | Recipient | Place Of Supply | Remarks |

| 1. | UAE | UAE | UAE | Domestic Supply Standard Rate 5% or ZeroRated/exempt in UAE |

| 2. | UK | UAE | UAE | Reverse Charge in UAE |

| 3. | UAE | KSA | KSA | Reverse Charge in KSA |

| 4. | Sharjah | Dubai | UAE | Standard Rate 5% or Zero-Rated/exempt in UAE |

| 5. | KSA | UAE | UAE | Reverse Charge in UAE |

Import of services in UAE from outside GCC

If the supplier is a non-UAE resident who provides service to a VAT-registered resident in the UAE, then the place of supply is the UAE.

Installation

The place of supply for installation services is where the installation is done.

Place of Supply Services – Reverse charge mechanism

In situations where a VAT registered person imports services into the UAE which would be subject to VAT if purchased in the UAE, the VAT registered purchaser has to account for VAT in respect of those supplies

Typically used for cross-border transactions to relieve a non-resident supplier from the requirement to register and account for VAT in the country of the purchaser

The purchaser will account for VAT on its normal VAT return and he may be able to claim that VAT back on the same return, subject to the normal VAT recovery rules

B2B Import of Services in UAE from outside of GCC

In relation to services, the place of supply is where the supplier has the place of residence subject to specific rules applying to real estate, transport, telecommunications, and cultural, artistic, sporting or similar activities. In cases where a VAT registered person imports services into the UAE which would be subject to VAT if purchased in the UAE, the VAT registered purchaser must account for VAT under the reverse charge mechanism.

The complication arises where goods are imported to the UAE and then transferred onwards to another GCC VAT implementing state. In this situation it has been mentioned that VAT must be paid using the reverse charge mechanism and the input VAT would not be reclaimed in the UAE but recovered in the GCC state which the goods were transferred to.

On the subject of the ability to recover the input tax, the conditions required include the following: the recipient must be a taxable person and must be VAT registered, VAT on the purchase must be correctly charged by the supplier, the services should be acquired by an eligible person, the recipient must receive and retain a tax invoice evidencing the transaction and the VAT to be recovered must have been paid.

When assessing the type of supply provided by logistics companies for VAT, it should be noted that the international transport of goods is a zero rated supply which means no VAT is charged on its service but input VAT can be recovered. These services include transport relating services for goods from a location in the UAE to a location outside the UAE, this transport would include the transport through the UAE and services supplied during the supply of transport services such as a handling fee

General services from a supplier in KSA to a customer in UAE

The VAT registered persons acquiring “Concerned Services” from KSA and will still be required to account for UAE VAT (where applicable) under the reverse-charge mechanism.

Concerned Services:

Services that have been imported where the place of supply is in the State, and would not be exempt if supplied in the State.

For customers not registered for VAT in the UAE, whether the “general” services they acquire from a supplier residing in KSA will be subject to 5% KSA VAT or 0% KSA VAT, will depend on whether KSA decides to apply a reciprocal transitional measure for services.

UAE businesses should now consider the impact of the transitional measure announced by FTA on their pricing, their system update and invoicing requirements for their transactions involving services supplied to / received from KSA

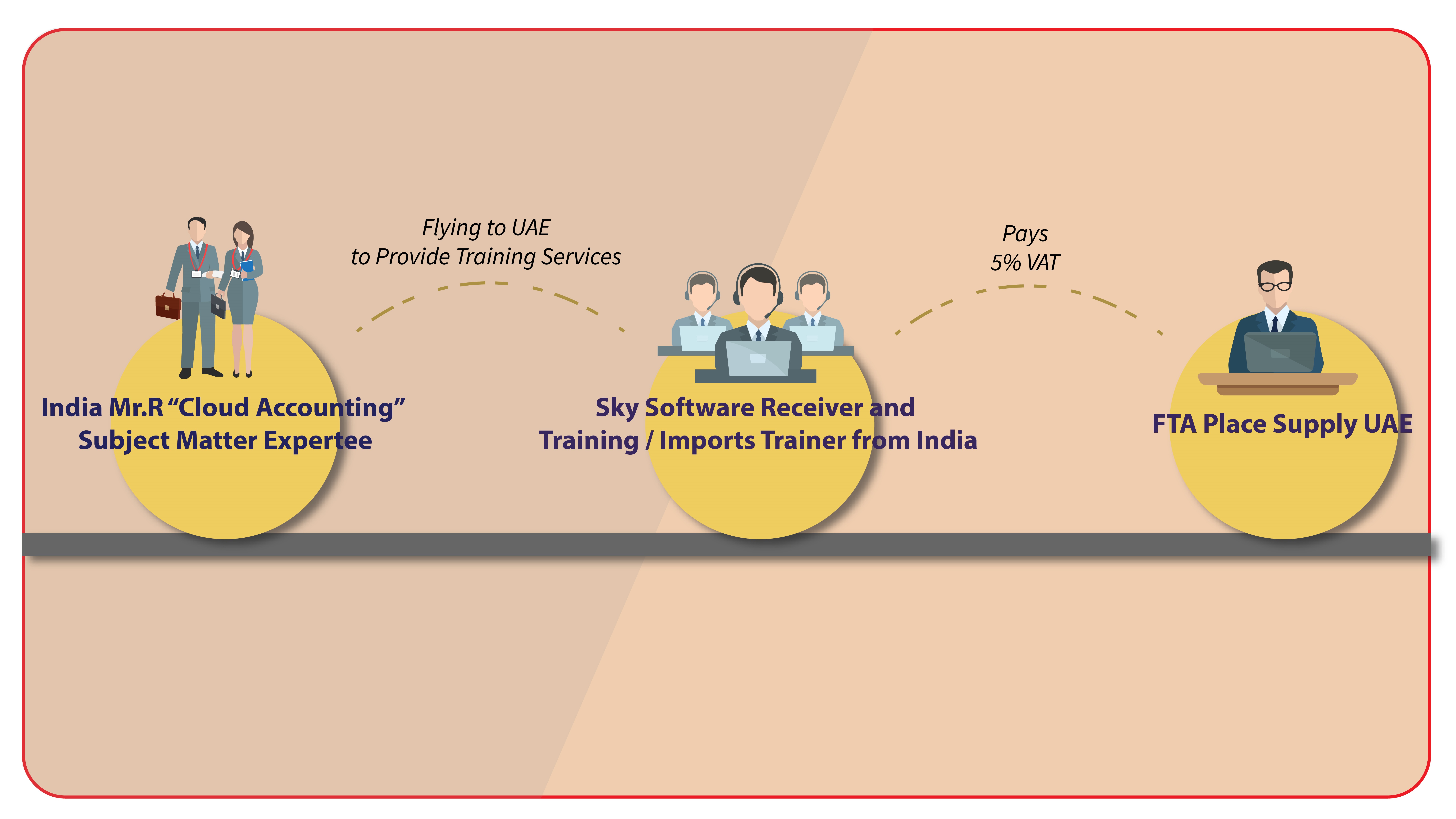

Example of Import Of Services in UAE

Mr. R residing in India provides online training to Sky Software Ltd in UAE Hence services are imported from India to UAE the place of supply is UAE VAT is payable. Mr. R is not registered in UAE therefore Sky Software Ltd is liable to pay 5%VAT to FTA under reverse charge mechanism.

Imports from the GCC countries:

Step 1: Company A located in Dubai posts an advertisement with a Saudi Local newspaper for the price of Saudi Riyals 30,000/-. For reference, KSA is part of the GCC countries to implement the VAT by 01-01-2018, but since the services rendered by the newspaper is on the Saudi soil and supplied to a UAE based company, it is not exempt from tax, hence the company levies a 5% VAT, so total invoice is 31,500/- SAR.

Step 2: : The GCC Tax treaty discuss the mechanism to be applied when goods and services are exchanged within the GCC. Assuming that the Saudi supplier invoice bears VAT, Company A will have to reclaim the VAT “input tax” back from the UAE authorities when it files the tax returns.

Step 3: This inter-country operation will have a currency exchange effect since it involves Saudi Riyals as a supply currency and UAE Dirhams as a local one. We believe that the authorities will disclose at some stage a currency exchange chart to streamline the conversions.

Assuming that 1 SAR equals to 0.98 AED, Company A will have to convert the VAT levied by the supplier from SAR to AED i.e. SAR 30,000 x 0.98 = 29,400 AED accordingly the VAT levied is 1,500 SAR x 0.98 = 1,470/- AED. Accordingly, Company A must claim 1,470 AED from the UAE authorities as an input tax.

Imports from non GCC countries:

Step 1: Company A located in Dubai posts an advertisement on Facebook for the price of US Dollars 30,000/-. Assuming that Facebooks has no representative in the UAE or the GCC to issue the invoices, the invoices will be sent from the US and bear no VAT.

Step 2: while submitting the tax returns, the mechanism to be used by Company A in such a case is the “reverse charge mechanism”.

Reverse charge rule: Since it is difficult to enforce the law against the import of services or other intangibles, as it does not pass through the country’s customs. Input VAT on imported services is self-assessed by the recipient who can claim it in reverse (a reverse charge). The reverse charge mechanism moves the responsibility for the reporting of a VAT transaction from the seller to the buyer of a good or service.

Assuming that 1 US Dollar equals to 3.675 UAE Dirhams, the Facebook invoice of 30,000 US$ equals to 110,250/- AED. Upon submission of its tax returns, Company A will disclose the purchase operation for the full amount at records the corresponding VAT (110,250 x 5%) as payable to the authorities and at the same time files the amount as an input tax to be claimed.

Company A which is the recipient of the service must report both its purchase (input VAT) and Facebook’s sale (output VAT) in its tax returns. The 2 declarations offset each other from a cash point of view, but the authorities will have full visibility of the transactions.

VAT on E-Commerce:

E-commerce or Electronic commerce being an online marketplace for goods and services in exchange for payments that can be done by transferring the amount to the supplier or via a direct card payment.

VAT on this type of business varies immensely from other economical activities due to the digital reality involved. To simplify the process, let us take the example of Souq.com which is an online platform selling a huge variety of items and acting as an agent for a big number of sellers. It is a known fact that the majority of the items displayed on the website does not belong to Souq.com, but to smaller retailers.

Although the end user pays directly through the website’s payment procedure, it is the seller himself who is the ultimate beneficiary.

Tracking the VAT through this complex channel will be a big challenge to the authorities since the European countries are still struggling to audit the digital marketplace. Check www.vatfraud.org a site made by online sellers to describe how they are victimized by other fellow sellers that bent the law to avoid the VAT.

It is worth mentioning that the digital platform is not the place of supply of the goods, as the goods will be moving from an actual warehouse and delivered to the client, we need to consider the below scenarios:

Step 1: Company A located in Dubai posts an advertisement on Facebook for the price of US Dollars 30,000/-. Assuming that Facebooks has no representative in the UAE or the GCC to issue the invoices, the invoices will be sent from the US and bear no VAT.

Step 2: while submitting the tax returns, the mechanism to be used by Company A in such a case is the “reverse charge mechanism”.

Reverse charge rule:

Since it is difficult to enforce the law against import of services or other intangibles, as it does not pass through the country’s customs. Input VAT on imported services is self-assessed by the recipient who can claim it in reverse (a reverse charge). The reverse charge mechanism moves the responsibility for the reporting of a VAT transaction from the seller to the buyer of a good or service.

Assuming that 1 US Dollar equals to 3.675 UAE Dirhams, the Facebook invoice of 30,000 US$ equals to 110,250/- AED. Upon submission of its tax returns, Company A will disclose the purchase operation for the full amount at records the corresponding VAT (110,250 x 5%) as payable to the authorities and at the same time files the amount as an input tax to be claimed.

Company A which is the recipient of the service must report both its purchase (input VAT) and Facebook’s sale (output VAT) in its tax returns. The 2 declarations offset each other from a cash point of view, but the authorities will have full visibility of the transactions.

The VAT on the online services will have pretty much the same process except in the case of import from a non-GCC member state. Reverse charge mechanism will have to be applied unless the importing party is not registered for VAT.

Accounting Entry for Import Of Services in UAE

| Particulars | Dr | Cr |

| Service Fee | 1,000,000 | |

| Input tax on Import | 50,000 | |

| To Service Provider | 1,000,000 | |

| To output on Import | 50,000 |

Reach Accountant Online Video learning for Import of services in UAE

Conclusion

When assessing the VAT on imports and exports, the first concept to grasp will be identifying the place of supply. This is important because it will deem whether VAT is due on that transaction or not. According to the FTA, if the supply is treated as made outside the UAE, then no UAE VAT is due, however if the supply is treated as made in the UAE, then VAT may be charged.

Popular posts

Related Blogs