Tax Invoice-with Excel and Word download

Introduction

Tax invoice is issued for taxable supply of goods & services. Tax invoice majorly contains details like description, quantity, value of goods/service, tax charged thereon and other particulars as may be prescribed.

Contents of the post

- Why tax invoice is required?

- Conditions to be met to issue tax invoice?

- Details to be furnished in Tax Invoice

- Generating a tax invoice using Reach Accountant Software

- Tax Invoice format with Excel/ Word download

- Who can issue a tax invoice?

- Transitional rules

Why Tax Invoice is required?

A tax invoice is a special type of invoice, which contains specific information needed for the effective operation of the VAT system. Tax invoice is one of the most important documents as

- It triggers the time of supply as the invoice date will determine when VAT is to be accounted for by a registered person on the supply of goods and services (accounting on invoice basis);

- determine which supplies made by him should be included in a particular taxable period;

- determine when he may claim his input tax based on the tax invoice received from his supplier;

- Tax invoices are important because they record creditable acquisitions for which an input tax credit can be claimed. Thus Tax invoice is a primary evidence for recipient to claim input tax credit of goods & service

As per FTA all invoices should display TRN Number of the organization. FTA has developed a VAT TRN Verification portal to check the validity of the TRN Numbers you receive from your business partners and suppliers.

Conditions to be met to issue Tax Invoice

Tax Invoice is the important and necessary document to be issued by a registrant when a taxable supply of goods or services is made. Under VAT in UAE, a Tax Invoice is to be issued by all registrants for taxable supplies to other registrants, where the consideration for the supplies exceeds AED 10,000.Hence, 2 conditions to be met for issuing a Tax Invoice are:

1.The recipient should be registered &

2.The consideration for the supplies should exceed AED 10,000

Details to be furnished in a Tax Invoice

- The words “Tax Invoice” clearly displayed on the invoice.

- The name, address, and Tax Registration Number of the Registrant making the supply.

- The name, address, and Tax Registration Number of the Recipient where he is a Registrant

- A sequential Tax Invoice number or a unique number which enables identification of the Tax and the order of the Tax Invoice in any sequence of invoices.

- The date of issuing the Tax Invoice.

- The date of supply if different from the date the Tax Invoice was issued.

- A description of the Goods or Services supplied.

- For each Good or Service, the unit price, the quantity or volume supplied, the rate of Tax and the amount payable expressed in AED.

- The amount of any discount offered.

- The gross amount payable expressed in AED.

- The Tax amount payable expressed in AED together with the rate of exchange applied where currency is converted from a currency other than the UAE dirham.

- tax invoice for which tax payment has been deferred for future date -Where the invoice relates to a supply under which the Recipient of Goods or Recipient of Service required to account for Tax, a statement that the Recipient is required to account for Tax, under Article 48 of the VAT Law should be given in the Tax Invoice

GENERATING A TAX INVOICE UNDER REACH SOFTWARE

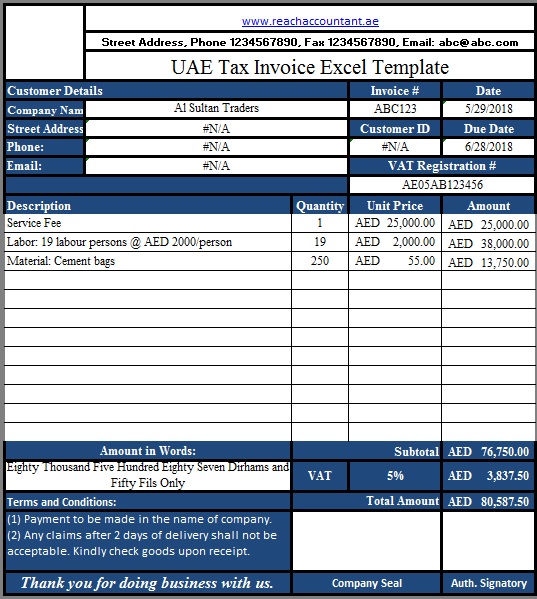

TAX INVOICE FORMAT – EXCEL AND WORD DOWNLOAD

WHO CAN ISSUE A TAX INVOICE

Issuance of Tax Invoice by Recipients of Goods and Services under UAE VAT

It should be noted under certain conditions and circumstances the recipient of good and service could issue tax invoice and Where a Recipient agrees to raise a Tax Invoice on behalf of a Registrant Supplier in respect of a supply of Goods or Services, that document shall be treated as if it had been issued by the supplier if the following conditions are to be met with;

- The Recipient of the Goods or Services is a Registrant

- The supplier and the Recipient agree in writing that the supplier shall not issue a Tax Invoice in respect of any supply to which this Clause applies

- The Tax Invoice shall contain the particulars required under law for Tax Invoice.

- The words “Tax Invoice raised by buyer” are clearly displayed on the Tax Invoice

If the supply is in a currency other than the UAE Dirham, then for the purposes of the Tax Invoice, the amount stated in the Tax Invoice shall be converted into the UAE Dirham according to the exchange rate approved by the Central Bank at the date of supply.

Issue of Tax Invoice by an Agent:

Where an agent who is a Registrant makes a supply of Goods and Services for and on behalf of the principal of that agent, that agent may issue a Tax Invoice in relation to that supply as if that agent had made the supply, and provided that the principal shall not issue a Tax Invoice.When the Tax Invoice relates to a supply for which the recipient should pay tax, a statement that the recipient is required to account for tax, under Article 48 of the VAT Law should be given in the Tax Invoice.

Foreign currency on Tax invoice

If the supply is in a currency other than the UAE Dirham, then for the purposes of the Tax Invoice, the amount stated in the Tax Invoice shall be converted into the UAE Dirham according to the exchange rate approved by the Central Bank at the date of supply.

Transitional Rules – Early invoicing or payment

Where an invoice is issued or payment is received prior to the date the VAT Law comes in to effect, the value of the payment/invoice will be subject to VAT where the following takes place after the date the VAT Law comes in to effect:

- Transfer of goods under the supplier’s supervision

- Goods are placed in the possession of the recipient of the goods

- Completion of assembly of the goods

- A customs statement is issued

- The customer accepts the supply of goods

The rules above are intended to avoid invoices being issued or payments being made prior to the effective date of the VAT law for supplies of goods which effectively take place after the effective date of the VAT law, for the purpose of avoiding tax

The mandatory details that have to be included in a tax invoice have been laid down in the VAT law and it is essential that all invoices issued under the VAT regime meet these requirements

Conclusion

If Tax Invoices issued do not contain the required information, it could lead to an Administrative Penalty. In this regard, it would be useful for all businesses to use a software which would automatically pick the details required in a Tax Invoice, notify the user if any mandatory details are not given in the Tax Invoice, generate the Tax Invoice quickly and most importantly, keep updated about all the details that are required to be given in a Tax Invoice. Ensuring that Tax Invoices are issued correctly by suppliers is also important for the recipient of the supply. The Tax Invoice serves as the basis on which the recipient can claim input tax deduction on the supply. Hence, businesses should take measures to ensure that Tax Invoices issued under VAT are accurate and complete.

Popular posts

Related Blogs