Margin scheme Invoice – Excel and Word Download

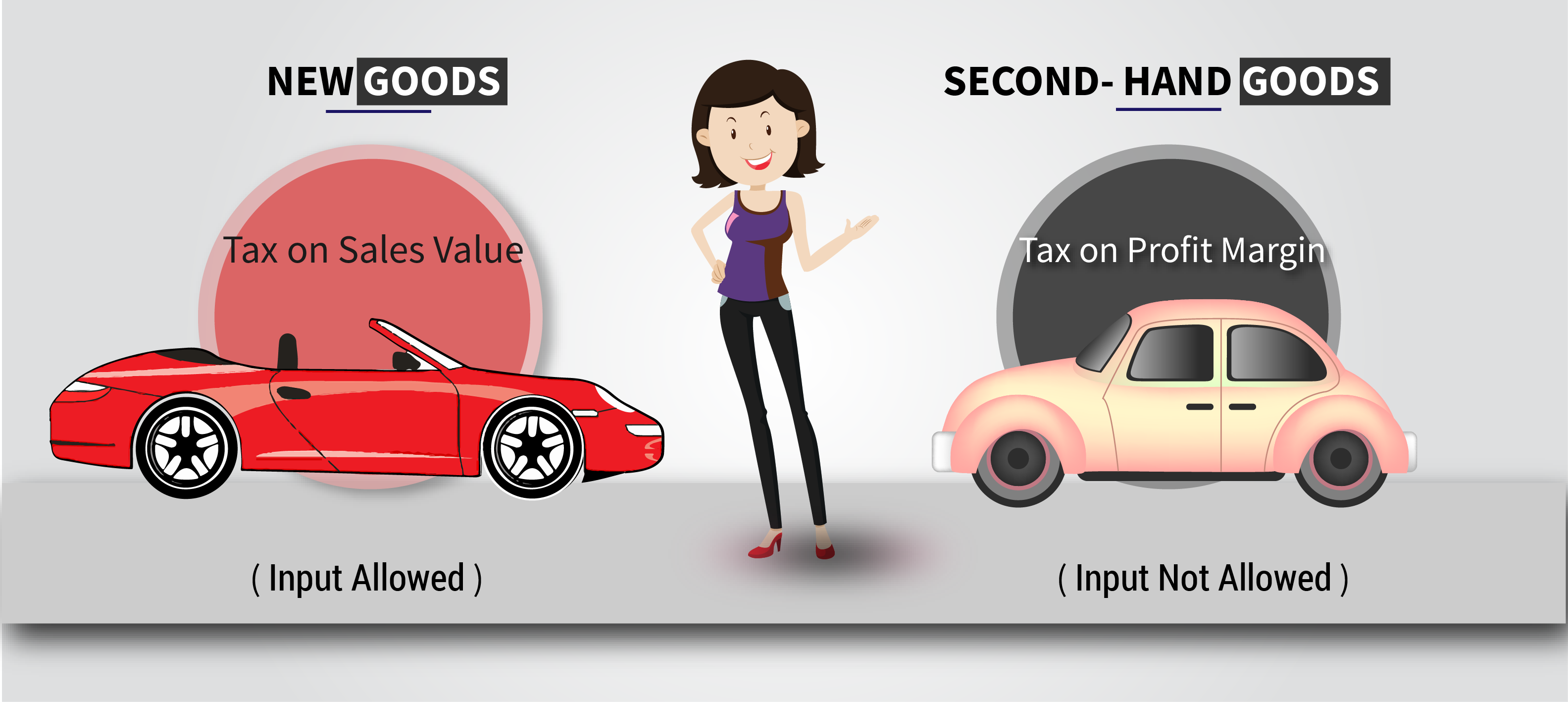

The VAT Margin scheme is designed to be used by VAT registered businesses that buy and sell secondhand goods, works of art, antiques and collector’s items. It allows the seller of such goods, under certain circumstances, to pay VAT to UAE Government only on the difference between the price he bought them for and the price he sold them for. It means tax on the profit margin earned on a supply, instead of the sale value. The Profit Margin Scheme is available only on supply of certain specified goods, not services. If you choose the profit margin scheme you will have to raise margin scheme Invoice appropriately

Whats in this post:

- Why is profit margin scheme needed?

- Who can opt for Profit Margin Scheme?

- Generating a Margin Scheme Invoice using Reach Accountant Software

- Margin scheme Invoice format with Excel/ Word download

- Conditions to be fulfilled if Margin Scheme is chosen

Why is Profit Margin Scheme needed?

When goods are purchased by registered second-hand goods dealers usually from unregistered consumers, VAT is not levied and hence, no input tax is recoverable by the second-hand goods dealer on the purchase. Hence, when these goods are sold by the second-hand goods dealers, it would not be right for the dealer to have to pay VAT on the full sale value, as it would lead to double taxation on the goods. As a result, for such supplies, a provision to pay VAT only on the profit earned on the supply has been given

Who can opt for Profit margin Scheme?

If you are selling any of the following goods, Profit Margin Scheme might apply to you

- certain second-hand goods

- works of art

- antiques and collector’s items

- second-hand vehicles and second-hand agricultural machinery acquired by dealers as stock-in-trade

Note: You also have the option to choose the normal scheme. If you choose not to operate the margin scheme, then the normal VAT rules apply.

Generating a Margin Scheme Invoice using Reach Accountant Software

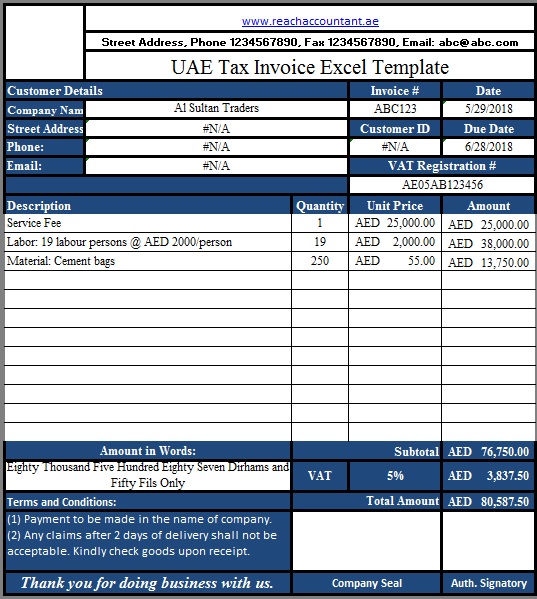

Margin Scheme Invoice Format – Excel and Word Download

Condition to be fulfilled if Margin Scheme is chosen

The supply of goods under the Profit Margin Scheme should fulfill either of the following conditions:

- They should be purchased from either a person who is not registered under VAT or a Taxable Person who supplied the goods under the Profit Margin Scheme OR

- Input tax should not be recovered on the purchase of the goods

Hence, in a nutshell, it is important that input tax should not be recovered on the goods supplied under the Profit Margin Scheme

Margin Scheme Invoices in UAE

To use the margin scheme, you must have invoices for each item that meet the VAT margin scheme requirements.

The margin scheme invoice requirements are not the same as general VAT invoice requirements.

You must have:

- an invoice from the seller when you bought the item

- a copy of the invoice you gave to the buyer when you sold the item

You must obtain a purchase invoice from the person you bought the item from which includes the following information:

- Date

- Seller’s name and address

- Your name and address, or that of your business

- The item’s unique stock-book number (if you bought the item from another VAT-registered business) • Invoice number (unless you made out the purchase invoice yourself)

- Item description

- Total price – you must not add any other costs to this price

- If you bought the item from another VAT-registered business, any of the following: ‘margin scheme – second hand goods’, ‘margin scheme – works of art’ or ‘margin scheme – collectors’ items and antiques

When you sell an item under the margin scheme your invoice must include:

- Date

- Your name, address and VAT registration number

- The buyer’s name and address, or that of their business

- The item’s unique stock book number

- Invoice number • Item description

- Total price – you must not show VAT separately

- Any of the following: ‘margin scheme – second hand goods’, ‘margin scheme – works of art’ or ‘margin scheme – collectors’ items and antique

A person supplying goods under the Profit Margin Scheme is not required to notify the FTA regarding the same. For the transactions which meet the criteria of the Profit Margin Scheme, the person can levy VAT accordingly and report such sales in the regular VAT return.

Popular posts

Related Blogs