Filing VAT Returns

Introduction

VAT Return, also known as ‘Tax return’ is a statement which a registered Entity needs to submit to the government authority. It is a formal documental declaration about income gained, loss incurred if any and VAT paid and levied on the total goods and services sold for the mentioned quarterly period or monthly and remitted to government. Details of Filing VAT Return Form are given below.

Driving factors from the post

- Who should file VAT Return in UAE?

- Submission of VAT Return in UAE

- Insight view of VAT Return form-Download

- Process for filing VAT Return in UAE

- Points to Remember

Who should file VAT Return in UAE?

A company whose annual turnover is equal or above AED 375000 should register itself under the Federal Law for filing VAT Return. If the Annual Turnover is between AED 187,500 & AED 375,000/, it is optional for the company to be registered under UAE VAT law. Further, if it is less than AED 187,500/, the company need not register under this law for filing VAT Return..

Submission of VAT Return in UAE

UAE taxpayers registered under VAT should file VAT returns with the Federal Tax Authority (FTA) on a quarterly basis. Returns must be filed as per the procedures specified in the VAT legislation, within 28 days from the end of the tax period. FTA can decide some type of businesses to file the VAT return on monthly basis to avoid the risk of tax evasion and improve the monitoring of compliance adherence by the business. Taxpayers can file their returns online using e-services. If the due date falls on a weekend or a national holiday, the deadline is extended to the first business day thereafter .Late filing of VAT return is penalized with AED 1,000 for the first time of occurrence of a delay. The penalty would be increased for subsequent non-compliance of filing of VAT Return.

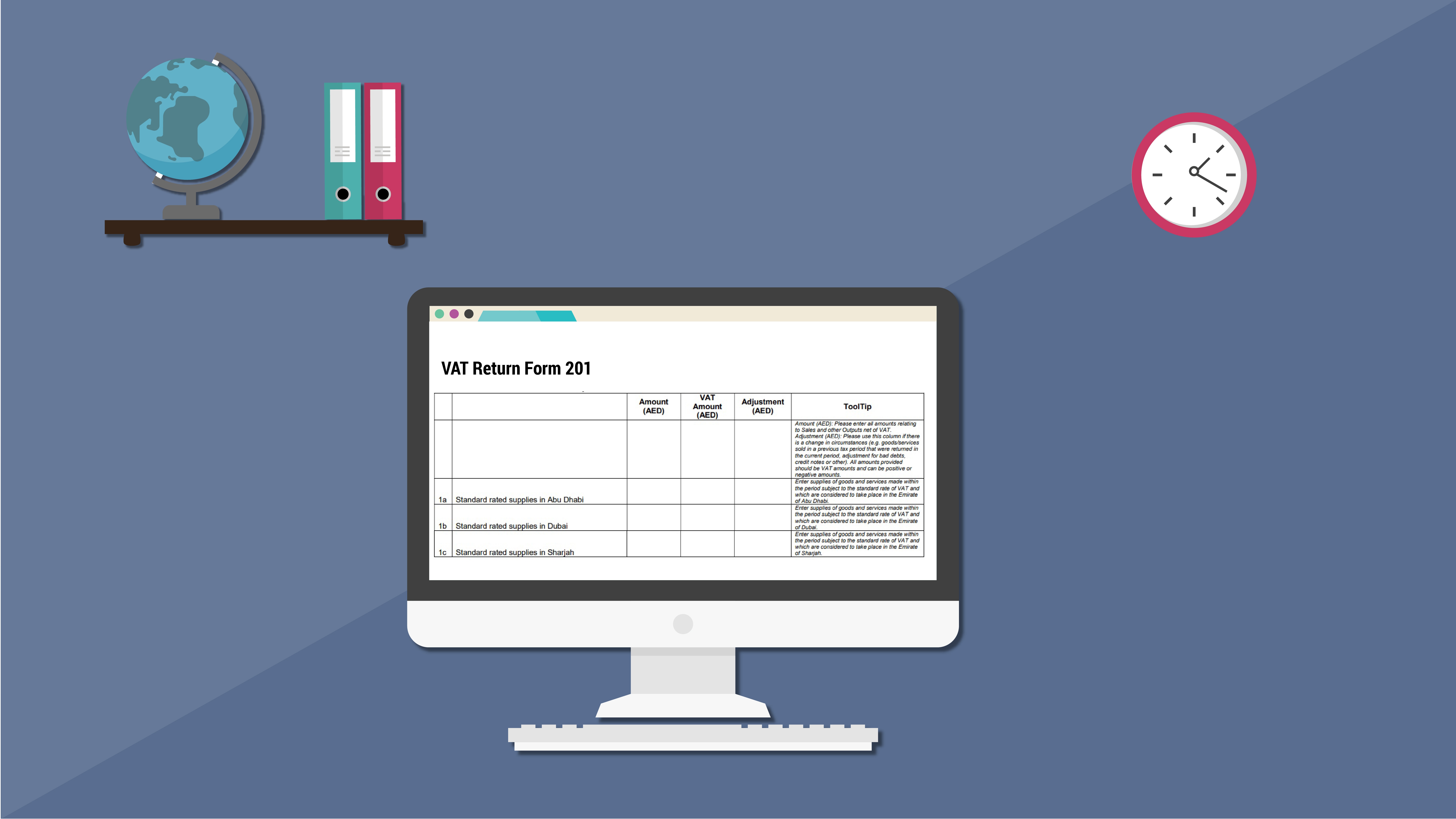

Insight view of VAT Return form

Federal Tax Authority has published the VAT Return Format in their web site “VAT201- VAT Return”. In order to access it, you have to login to the FTA e-services portal using your registered username and password. The taxpayer needs to fill and submit in order to complete the VAT Return filing.

The Form VAT 201 is classified into 7 sections as mentioned below:

- Details of Taxable Person

- VAT Return Period

- VAT on sales and all other outputs

- VAT on expenses and all other inputs

- Net VAT Due

- Additional reporting requirements

- Declaration and Authorized Signatory

Each of these sections contain various boxes in which the taxpayer needs to furnish the details in order to complete the VAT Tax return filing.

Process for filing VAT Return in UAE

Step 1: Login to Federal Tax Authority portal at www.tax.gov.ae with the registered user name and password.

Step 2: Click on VAT 201 – New VAT Return option under the e-services section of the portal to open the VAT Return form.

Step 3. Fill the details of standard rated supplies from box 1a to 1g.

All Standard Rated Supplies should be reported Emirate wise for VAT Return Filing. For example: if a company has Head Office in Dubai and a branch in Abu Dhabi, all the sales made from Dubai HO will be reported as Dubai Sales (1b) and all sales from Abu Dhabi Branch will be reported as Abu Dhabi Sales (1c).

Even though delivery of material is happening in different Emirates, the above reporting doesn’t change. For non-established businesses in the UAE, supplies have to be reported in the Emirate where the supply is received.

For example, if the company sells AED 2,000,000/- from Dubai Office and AED 700,000/- from Abu Dhabi Office the respective amount without VAT will be showing as sales under amount column. AED 100,000/- will be showing as VAT against the Dubai Sales and AED 35,000/- will be showing as VAT against Abu Dhabi sales.

Details to be furnished under Taxable Supplies is as follows

- Value of supply of goods and services (net of discount).

- Value of sale of commercial Property

- Advances receivedif any

- Deposits received other than those which are refundable (e.g- security deposit)

- Sale of goods under Profit Margin Scheme.

- Goods supplied within Designated Zone and are used within Designated Zone

- Supplies by a non-resident who is registered in UAE as the recipient of goods or services is not registered in UAE (and hence Reverse Charge Mechanism does not apply).

- Credit notes issued (to be deducted from total supplies).

Deductions of errors of previous Tax periods provided the error does not result in the Output Tax being increased/decreased by an amount more than AED 10,000/. Self-declaration issued by the registrant separately and hence the same cannot be included for the VAT Return Filing.

Notes:

- Supply value should be net figure i.e. excluding the VAT charged to the customer, which is to be included in the next column.

- Goods sold under Profit Margin Scheme, the full value of such supplies should be reduced by the value of VAT calculated on the margin.

- Adjustment column shown on the VAT return should only be used to adjust the TAX due relating to the following;

- VAT Bad Debt Relief

- Sales of taxable commercial property in the UAE where tax is paid by the customer.

Step 4: Treatment of Tax Refunds provided to Tourists

Retailers providing refund to tourists under the official tourist refund scheme should provide the details regarding the same in the VAT Return Filing form.

Step 5: Supplies subject to the reverse charge provisions.

The value of supplies of goods and services under Reverse Charge Mechanism should be declared separately. The value of goods imported into UAE will be auto-generated to the extend it was declared under the Taxable Person’s customs registration number.

Goods imported through UAE customs will be reported under Goods imported into the UAE header. In this step services which are imported during the period will be included. For example, if the company has received a service from a software firm located outside UAE worth AED 100,000/-, 5% VAT i.e. AED 5,000/- will be shown as Output VAT under this step. However, the same amount can be taken as input under Supplies subject to the reverse charge provisions header provided other provisions of the law is met.

Step 6: Zero-rated supplies

All the supplies made under zero rated vat (“zero-rated supplies”). Since, the VAT on supply is calculated at Nil, only the net value of the supply should be stated here. For example, if the company exports goods to outside UAE worth AED 1,000,000/- the sales value will be shown under this box.

Step 7: Exempt supplies

Only the exempted supplies made during the period are shown. As there is no VAT on such kind of supplies, only the net value of the supply is to be stated in this Box.

Step 8: Goods imported into the UAE

Details goods imported through UAE customs should be furnished .The aggregate of customs declared value (CIF) and the customs duty amount will be the value of import. This amount of import will include the excise duty as well if the product is taxable under Excise law. 5% tax on above has to be shown as tax payable. This amount will be automatically generated in VAT Return form.

Agents importing goods into the UAE on behalf of the non- registered persons are responsible to pay tax for the import of goods.

The value input credit should be calculated and same to be included under Supplies subject to the reverse charge provisions header for VAT calculation

Step 9: Adjustments to goods imported into the UAE

Any corrections or omissions on the figure disclosed under Goods imported into the UAE header can be rectified by using Adjustments to goods imported into the UAE section Adjustments is allowed to the value of imported goods which is auto-populated in case of omission or mistake in the value when compared to the amount reported in the customs and import declaration. Any import of goods which are not subject to standard rate of VAT in the UAE at 5% can also be adjusted as the imports are assumed to be subject to 5% VAT rate. The figures could vary from positive to negative figures but when questioned by the FTA should be answerable.

For agents who imports goods into the UAE on behalf of non- registered persons, it is the agents’ responsibility to pay tax for the import of goods. Any corrections or amendments to the value can also be done at this stage.

Step 10: Standard rated expenses

All the expenses pertaining to the standard VAT rate to recover the Input Tax. It is inclusive of purchase of goods from the local market as well. The total amount of the purchase and expenses made for which Input Tax has to be claimed should be stated in the “Amount (AED)” column. This should not include the tax element which is been paid to the suppliers or service providers, only net of tax. This column should only include the VAT recoverable and not the total value of VAT for which cost has been incurred.

Summarized Points

- Goods or services purchased (net of discount).

- Goods or services purchased before Tax Registration for which input Tax can be claimed.

- Credit notes raised by the supplier.

- Errors noted for the Previous Tax periods can be deducted provided the error does not result in the Output Tax being increased/decreased by an amount more than AED 10,000/.

Notes:

- Total net value of the standard rated expenses on which the taxpayer is seeking to recover VAT should be included while declaring the standard rated expenses.

- The VAT column should include only those amounts which you are entitled to recover.

- Adjustment column to be used to adjust the Tax amount for the following;

- VAT Bad Debt Relief

- Input Tax apportionment annual adjustments

- Capital Asset Scheme adjustments

In case of errors where self-declaration is required as mentioned above, the same procedure should be followed.

Step 11: Supplies subject to the reverse charge provisions

Any output tax payable under the reverse charge mechanism that has been stated in Supplies subject to the reverse charge provisions. Goods imported into the UAE and Adjustments to goods imported into the UAE, can be recovered in this stage after being calculated. Any expenses where VAT is incurred and falling under Reverse Charge Mechanism for which Input Tax is not recoverable, those expenses should not be stated here. If you have paid VAT during import due to any reason, such VAT amount also can be mentioned for reimbursement.

Step 12: Calculation of due tax or recoverable tax for the period

The difference between output vat and input vat is the amount payable the authority during the period.If the Output Tax figure is more that the Input Tax figure, there is a provision of being refunded for the net amount of recoverable tax. If the tax payer do not opt for refund of the excess sum, the same can be carried forward to subsequent Tax Period which can be adjusted for Tax payable or penalties or can be applied for tax refunds in future date.

Step 13: Refund of excess recoverable tax.

The Option for net recoverable tax will be available on VAT return for recovery of excess tax. There will be two options ‘YES’ & ‘NO’.

If you select ‘YES’, kindly fill and complete the VAT Refund Form VAT 311 once VAT Return Form is submitted.

If you select ‘No’ your excess tax amount to be recovered will be taken forward for Subsequent Tax Period which can be used to pay for subsequent tax period or penalties.

Step 14: Confirmation mail on the submission of the VAT Return Form.

The VAT Return form can be saved as a draft in between and can be continued at later point of time. Ensure all the details entered are correct and true before submitting the VAT Return form,. Upon clicking submit button of VAT Return Form an email will be received for confirming the same.

Step 15: How will you pay VAT?

Steps for paying VAT liability and administrative penalties are below:

1.Go to “My Payments”

- .Enter the figure that you should pay and click “Make Payment”.

.You will then be directed to ‘Payment Information’ screen to proceed with the payment. Click on ‘Pay Now’ button to be directed to e-Dirham gateway

You may pay using the e-Dirham payment gateway which supports payments through an e-Dirham card or a credit card (Visa and MasterCard only) or GIBAN. A payment using an e-Dirham card will typically incur a charge of AED 3, while a payment using a credit card will typically incur a charge between 2% – 3% of the total payment amount

The following should be taken care while filing VAT Return :

When completing each step of the VAT Return, you must:

- All amount should be in United Arab Emirates Dirhams (AED).

- All amounts should be rounded off to the nearest fills.

- All mandatory fields should be completed.

- Use “0” if there are no amounts to be declared.

DOWNLOAD VAT RETURN FORM VAT 201

Points to Remember

- VAT Return Form VAT 201

- Input refund form VAT 311

- The return can be submitted by the Taxable Person, or another person who has authority to do so on behalf of the taxable person (for example, a Tax Agent or a Legal Representative)

- If the due date for the submission of the VAT Return and the corresponding payment falls on a weekend or a national holiday, the deadline for filing the VAT Return or making a payment is extended to the first business day thereafter

- If there is no business transaction for the Tax Period, you are required to submit a “nil” VAT Return by the respective due date

- Once the date of the supply has taken place, the Taxable Person must account for the output tax in the VAT Return covering that Tax Period

- Supplies within Designated Zone, out of scope supplies and disbursements are not required to be reported in VAT return

- Adjustments can be made in the pre-populated VAT amount on import of goods in case there is any error at customs end

- For an excess amount, one can either apply for refund for that tax period in Form VAT 311 or can carry forward that amount to next period

- VAT Returns must be submitted within the specified deadline, otherwise, a penalty of AED 1,000 will be imposed for the first time of occurrence of a delay. In case of repetitive non-compliance within 24 months, the penalty will be increased to AED 2,000 for each offense

- If one do not submit a VAT Return by the specified due date, the FTA may issue a tax assessment to you with an estimate of the payable tax. In such a case, you may be required to pay any payable tax assessed, penalty on non-submission of tax return and/or late payment penalty upon the issuance of the tax assessment (as applicable).

- Tax needs to be paid after the submission of VAT return but within the due date for that tax period; and

- Following the submission of a VAT Return, the reported Payable Tax must be settled within the deadline. Failure in the payment before the due date would result in a late payment penalty consisting of:

- (2%) of the unpaid tax immediately levied once the payment of Payable Tax is late

- (4%) is due on the seventh day following the deadline for payment, on the amount of tax which is still unpaid

- (1%) daily penalty charged on any amount that is still unpaid one calendar month following the deadline for payment with an upper ceiling of (300%)

Conclusion

As the VAT Return is to be filed every quarterly,it becomes imperative to make use of accounting software to upload the return files.Reach Online VAT Accounting Software is designed to suit your business needs.It is FTA approved VAT Accounting Software,with all the features to run the business operations smoothly.

Popular posts

Related Blogs