Filing VAT Returns under Profit Margin Scheme

Introduction

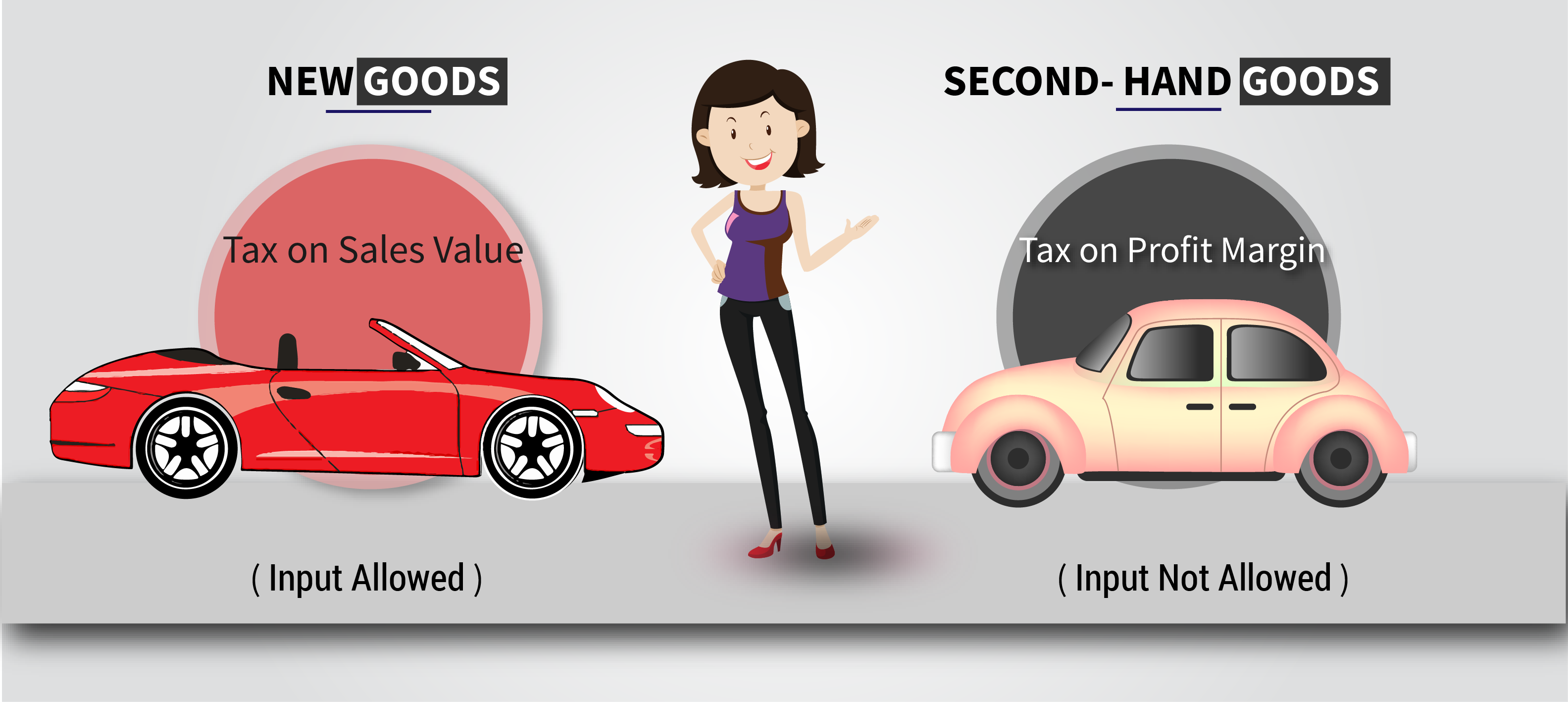

The margin scheme was introduced for reducing the effects of double taxation with regards to the sale of second-hand goods. It operates by allowing dealers in certain second-hand goods, works of art, antiques and collectors’ items to pay VAT on the difference between the sale price and the purchase price of the goods. The scheme can be chosen at the discretion of the dealers concerned. If the dealer chooses not to operate the margin scheme then the normal VAT rules apply. Therefore a taxable person filing VAT returns under profit Margin scheme has an option to calculate tax on the profit earned on a supply, instead of the sale value through Margin Scheme. The Profit Margin Scheme is applicable only on supply of certain specified goods, and not services. Thus filing VAT returns under profit margin scheme is possible only for goods.

What’s in the post?

- Goods supplied eligible for filing VAT returns under Profit Margin Scheme

- Margin Scheme Invoice for filing VAT returns under Profit Margin Scheme

- Eligibility for filing VAT returns under Profit Margin Scheme

- When you sell an item under the margin scheme your invoice must include

- How the margin scheme operates for filing VAT returns under Profit Margin Scheme

- Formula for calculating VAT payable for the purpose of Filing VAT returns under profit margin scheme

- Filing VAT Returns under Profit Margin Scheme in VAT Return Form 201

- Eligibility for claiming Input Tax Credit when filing VAT returns under profit margin scheme

- Conclusion

Goods supplied eligible for filing VAT returns under Profit Margin Scheme

The goods which can be supplied under the Profit Margin Scheme are:

- Second-hand goods, i.e. tangible moveable property which is suitable for further use as it is, or after repair

- Antiques, i.e. goods which are over 50 years old

- Collectors’ items, i.e. stamps, coins and currency

Margin Scheme Invoice for filing VAT returns under Profit Margin Scheme

An invoice issued by an accountable dealer in respect of a supply under the margin scheme must not show VAT separately. Any such invoice should be clearly endorsed ‘Margin Scheme – this invoice does not give the right to an input credit of VAT’.

To use the margin scheme, you must have invoices for each item that meet the VAT margin scheme requirements.

The margin scheme invoice requirements are not the same as general VAT invoice requirements.

You must have:

- an invoice from the seller when you bought the item

- a copy of the invoice you gave to the buyer when you sold the item

Eligibility for filing VAT returns under Profit Margin Scheme if

- You have bought the item from a non VAT registered business or individual or

- You have bought the item from a VAT registered business that is selling it to you under the margin scheme

You must obtain a purchase invoice from the person you bought the item from which includes the following information:

- Date

- Seller’s name and address

- Your name and address, or that of your business

- The item’s unique stock-book number (if you bought the item from another VAT-registered business)

- Invoice number (unless you made out the purchase invoice yourself)

- Item description

- Total price – you must not add any other costs to this price

- If you bought the item from another VAT-registered business, any of the following: ‘margin scheme – second hand goods’, ‘margin scheme – works of art’ or ‘margin scheme – collectors’ items and antiques

When you sell an item under the margin scheme your invoice must include:

- Date

- Your name, address and VAT registration number

- The buyer’s name and address, or that of their business

- The item’s unique stock book number

- Invoice number

- Item description

- Total price – you must not show VAT separately

- Any of the following: ‘margin scheme – second hand goods’, ‘margin scheme – works of art’ or ‘margin scheme – collectors’ items and antique

How the margin scheme operates for filing VAT returns under Profit Margin Scheme

The margin scheme provides that VAT is payable on the sale of margin scheme goods by reference to the difference between the sale price and the purchase price of the goods. This is illustrated as follows:

- Dealer’s sale price of goods AED 500

- less dealer’s purchase price AED 300

- Dealer’s Margin AED 200

Therefore the profit margin is the difference between the purchase price of the goods and the selling price of the goods.

Formula for calculating VAT payable for the purpose of Filing VAT returns under profit margin scheme

Tax amount = Value inclusive of tax * tax rate ÷ (100 + tax rate)

Example: A VAT registered second-hand goods dealer, Amaan Used Cars, purchases a used car from a consumer, Mr. Jaan. The purchase price is AED 20,000. After the required repairing and refurbishing, Amaan Used Cars supplies the car to another consumer, Mr. Roy, for AED 30,000.

Here, the profit margin of Amaan Used Cars on the supply is:

AED 30,000 – AED 20,000 = AED 10,000 (Selling price- purchase price).

The profit margin is inclusive of tax. Hence, the tax to be paid can be calculated as shown below: Value inclusive of tax = AED 10,000

Tax rate = 5%

Hence, tax amount= 10,000 * 5 / (100 + 5) = AED 476.

Scenario 2

Sales AED 2000

Purchases AED 3000

Negative margin AED 1,000 No VAT payable

Profit Margin Scheme is a good scheme for paying tax on supply of second-hand goods. The benefit of opting for the margin scheme is that the dealer needs to pay tax only on the margin earned on sale. This is very useful for dealers who mostly purchase used goods from end customers. As there is no applicability of input tax recovery on these purchases, these dealers need to pay tax only on the margin earned on sale. However, dealers opting for the scheme should ensure that input tax has not been recovered on the purchase of these goods.

Filing VAT Returns under Profit Margin Scheme in VAT Return Form 201

Additional Reporting Requirements Profit Margin Scheme

This applies to vendors who sell secondhand goods and have applied for the profit margin scheme, in which inputs are exempt from VAT and VAT is applicable only to the profit made during sales. Select yes if you have enrolled yourself under this scheme.You will be required to indicate whether you have used and applied the provisions of the Profit Margin Scheme during this period. Please select ‘Yes’ only if you have used the Profit Margin Scheme during the current Tax Period for which you are filing the current VAT Return.

Eligibility for claiming Input Tax Credit when filing VAT returns under profit margin scheme

When registered second-hand goods dealers purchases used goods from registered person, the supplier will levy VAT on the supply. If the second-hand goods dealer is opting for the margin scheme and filing VAT returns under profit margin scheme for supply of these used goods, the dealer is not eligible to recover the input tax paid. If the second-hand goods dealer is not opting for the margin scheme, then the dealer is eligible to recover the input tax paid.

Conclusion

The supply of goods under the Profit Margin Scheme should fulfil either of the following conditions:

- They should be purchased from either:

- A person who is not registered under VAT or

- A Taxable Person who supplied the goods under the Profit Margin Scheme

OR

- Input tax should not be recovered on the purchase of the goods

Hence, in a nutshell, it is important that input tax should not be recovered on the goods supplied under the Profit Margin Scheme.

Popular posts

Related Blogs