GST HELPLINE

GST is a single tax on the supply of goods and services, right from the manufacturer to the consumer. Credits of input taxes paid at each stage will be available in the subsequent stage of value addition, which makes GST essentially a tax only on value addition at each stage. The final consumer will thus bear only the GST charged by the last dealer in the supply chain, with set-off benefits at all the previous stages.

BENEFITS OF GST

Easy compliance:

Uniformity of tax rates and structures:

Removal of cascading:

Improved competitiveness:

Gain to manufacturers and exporters:

GST SOFTWARE

As GST is all set to bring a historic change in the indirect taxation system in India.A number of established as well as startup companies are emerging to support this new tax with a wide range of accounting software.

In fact,IT and software companies wish to see huge businesses in the coming days since a reliable and good GST Software is the backbone of the entire GST system.

Some of the popular GST accounting software names that we tend to hear these days are :

- ERP 9

- Cleartax GST Biz

- Zoho Books

- Quick books

- ProfitBooks

They have been equipped with features to help businesses and service providers follow proper accounting processes,make you GST compliant and adhere to the new provisions.There might be a lot more to add to the list.

GST TRAINING- GST HELPLINE

The salient features of GST are as under:

- The GST would be applicable on the supply of goods or services as against the present concept of tax on the manufacture and sale of goods or provision of services. It would be a destination based consumption tax.

- (ii) It would be a dual GST with the Centre and States simultaneously levying it on a common tax base. The GST to be levied by the Centre on intra-State supply of goods and / or services would be called the Central GST (CGST) and that to be levied by the States would be called the State GST (SGST).

- The GST would apply to all goods other than alcoholic liquor for human consumption and five petroleum products, viz. petroleum crude, motor spirit (petrol), high speed diesel, natural gas and aviation turbine fuel. It would apply to all services barring a few to be specified.

- Tobacco and tobacco products would be subject to GST. In addition, the Centre would have the power to levy Central Excise duty on these products.

- The GST would replace the following taxes currently levied and collected by the Centre: a. Central Excise duty b. Duties of Excise (Medicinal and Toilet Preparations) c. Additional Duties of Excise (Goods of Special Importance) d. Additional Duties of Excise (Textiles and Textile Products) e. Additional Duties of Customs (commonly known as CVD) f. Special Additional Duty of Customs (SAD) g. Service Tax h. Central Surcharges and Cesses so far as they relate to supply of goods and services

- State taxes that would be subsumed under the GST are:

- State VAT

- Central Sales Tax

- Luxury Tax

- Entry Tax (all forms)

- Entertainment and Amusement Tax (except when levied by the local bodies)

- Taxes on advertisements

- Purchase Tax

- Taxes on lotteries, betting and gambling

- State Surcharges and Cesses so far as they relate to supply of goods and services

- The CGST and SGST would be levied at rates to be jointly decided by the Centre and States. The rates would be notified on the recommendations of the GST Council.

- There would be a floor rate with a small band of rates within which the States may fix the rates for SGST.

- The list of exempted goods and services would be common for the Centre and the States.

- Tax payers with an aggregate turnover in a financial year up to [Rs.10 lakhs] would be exempt from tax. [Aggregate turnover shall include the aggregate value of all taxable and non-taxable supplies, exempt supplies and exports of goods and/or services and exclude taxes viz. GST.] Aggregate turnover shall be computed on all India basis. For NE States and Sikkim, the exemption threshold shall be [Rs. 5 lakhs]. All taxpayers eligible for threshold exemption will have the option of paying tax with input tax credit (ITC) benefits. Tax payers making inter-State supplies or paying tax on reverse charge basis shall not be eligible for threshold exemption.

- Small taxpayers with an aggregate turnover in a financial year up to [Rs. 50 lakhs] shall be eligible for composition levy. Under the scheme, a taxpayer shall pay tax as a percentage of his turnover during the year without the benefit of ITC. The floor rate of tax for CGST and SGST shall not be less than [1%]. A tax payer opting for composition levy shall not collect any tax from his customers. The composition scheme is optional. The eligible taxpayers shall have the option of paying tax with ITC benefits. Tax payers making inter-State supplies or paying tax on reverse charge basis shall not be eligible for composition scheme.

- An Integrated GST (IGST) would be levied and collected by the Centre on interState supply of goods and services. Accounts would be settled periodically between the Centre and the States to ensure that the SGST portion of IGST is transferred to the destination State where the goods or services are eventually consumed.

- Tax payers shall be allowed to take credit of taxes paid on inputs (input tax credit) and utilize the same for payment of output tax. However, no input tax credit on account of CGST shall be utilized towards payment of SGST and vice versa. The credit of IGST would be permitted to be utilized for payment of IGST, CGST and SGST in that order.

- HSN (Harmonised System of Nomenclature) code shall be used for classifying the goods under the GST regime. Taxpayers whose turnover is above Rs. 1.5 crores but below Rs. 5 crores shall use 2 digit code and the taxpayers whose turnover is Rs. 5 crores and above shall use 4 digit code. Taxpayers whose turnover is below Rs. 1.5 crores are not required to mention HSN Code in their invoices.

- Exports shall be treated as zero-rated supply. No tax is payable on export of goods or services but credit of the input tax related to the supply shall be admissible to exporters and the same can be claimed as refund by them.

- Import of goods and services would be treated as inter-State supplies and would be subject to IGST in addition to the applicable customs duties. The IGST paid shall be available as ITC for further transactions.

- The laws, regulations and procedures for levy and collection of CGST and SGST would be harmonized to the extent possible.

- GST and Centre-State Financial Relations

- Currently, the fiscal powers between the Centre and the States are clearly demarcated in the Constitution with almost no overlap between the respective domains. The Centre has the powers to levy tax on the manufacture of goods (except alcoholic liquor for human consumption, opium, narcotics etc.) while the States have the powers to levy tax on the sale of goods. In the case of inter-State sales, the Centre has the power to levy a tax (the Central Sales Tax) but, the tax is collected and retained entirely by the States. As for services, it is the Centre alone that is empowered to levy service tax. National Academy of Customs Excise and Narcotics (NACEN)

4.1 Introduction of the GST would require amendments in the Constitution so as to simultaneously empower the Centre and the States to levy and collect this tax. The assignment of simultaneous jurisdiction to the Centre and the States for the levy of GST would require a unique institutional mechanism that would ensure that decisions about the structure, design and operation of GST are taken jointly by the two. For it to be effective, such a mechanism also needs to have Constitutional force.

Input tax credit

The provisions of input tax credit have been prone to litigation. The Model GST law provides an elaborate mechanism for availment and utilization of ITC and seeks to impart clarity with a view to minimizing disputes. The important provisions of the law are as under:

- Tax payer is allowed to take credit of taxes paid on inputs (input tax credit), as selfassessed, in his return.

- Taxpayer can take credit of taxes paid on all goods and services, other than a few in the negative list, and utilize the same for payment of output tax.

- Credit of taxes paid on inputs can be taken where the inputs are used for business purposes or for making taxable supplies.

- Full input tax credit shall be allowed on capital goods on its receipt as against the current Central Government and many State Government practice of staggering the credit in two or three equal instalments.

- Unutilized input tax credit can be carried forward.

- The facility of distribution of input tax credit for services amongst group companies has been provided for through the mechanism of Input Service Distributor (ISD).

Refund

Refund provisions have been simplified and made more taxpayer friendly. Some of the important provisions of the Model GST Law are as under: National Academy of Customs Excise and Narcotics (NACEN) Page 11

- Time limit for claiming refund has been increased from one year to two years.

- Refund claim along with documentary evidence is to be filed online without any physical interface and the tax refund will be directly credited to the nominated bank account of the applicant. Besides, refund of inadvertent/excess payment can be claimed through return also.

- Refund shall be granted within 90 days from the date of receipt of complete application. Interest is payable if refund is not sanctioned within the stipulated period of 90 days.

- If the refund claim is less than Rs. 5 lakhs, there is no need for the claimant to furnish any documentary evidence that he has not passed on the incidence of tax to any other person. Only a self-certification to this effect would suffice.

- Refund of input tax credit shall be allowed in case of exports or where the credit accumulation is on account of inverted duty structure (i.e. where the tax rate on output is higher than that on inputs).

- In case of refund claim on account of exports, 80% of the claim shall be paid immediately on a provisional basis without verification of documentary evidence.

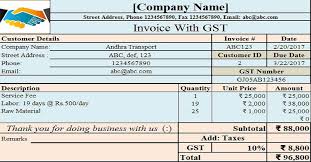

GST HELPLINE -INVOICING

Under GST invoicing rules and formats have been notified covering details such as supplier’s name, shipping and billing address, HSN Code, place of supply, rate. In this article we will be covering all aspects of invoicing under GST.

Time limit to for invoicing under GST

The GST Model law has defined the time limit for issue of GST tax invoices, revised bills, debit notes and credit note.

Following are the due dates for issuing an invoice to customers:

- Supply of Goods (Normal case)- On or before date of removal/ delivery

- Supply of Goods (Continuous Supply)- On or before date of issue of account statement/ payment

- Supply of Services (General case)- within 30 days of supply of services

- Supply of Services (Banks & NBFCs)- within 45 days of supply of services

Revise Already Issued Invoices under pre-GST regime

Revised tax invoices can be issued by a registered taxable person within one month from issuance of certificate of registration i.e. GST Registration. It will be issued against the invoice already issued during the period starting from the effective date of registration till the date of issuance of certificate of registration to him

What is Bill of Supply?

Tax invoice is generally issued to charge the tax and pass on the credit. In GST there are some instances where the supplier is not allowed to charge any tax and hence a Tax invoice can’t be issued instead another document called Bill of Supply is issued.

How to raise aggregate invoices?

Where the value of invoice is less than Rs 200 and the recipient is an unregistered, registered taxpayer, he or she can issue an aggregate invoice for such multiple invoices on a daily basis.

For example, you may have issued 3 invoices in a day of Rs.80, Rs90 and Rs120. In such a case you can issue a single invoice, totaling to Rs290, to be called an aggregate invoice.

When is debit note issued?

Debit note is to be issued by supplier:

- Original tax invoice has been issued and taxable value in the invoice is less than actual taxable value.

- Original tax invoice has been issued and tax charged in the invoice is less than actual tax to be paid.

When is credit note issued?

Credit note is to be issued by supplier:

- Original tax invoice has been issued and taxable value in the invoice exceeds actual taxable value.

- Original tax invoice has been issued and tax charged in the invoice exceeds actual tax to be paid.

- Recipient refunds the goods to the supplier

- Services are found to be deficient

What are the specific mandatory fields in an GST compliant invoice?

To issue and receive a GST compliant invoice is a prerequisite to claim ITC. If a taxpayer does not issue such invoice his customer loses ITC claim and the taxpayer loses its customers. Here we mention the mandatory fields in an invoice:

- Invoice number and date

- Customer name

- Shipping and billing address

- Customer and taxpayer’s GSTIN

- Place of supply

- HSN code

- Taxable value and discounts

- Rate and amount of taxes i.e. CGST/ SGST/ IGST

- Item details i.e. description, unit price, quantity

What are the various types of invoices or supporting documents?

All different types of GST compliant invoices such as:

- sales invoices

- purchase invoices

- bill of supply

- credit notes

- debit notes

- advance receipts

- refund vouchers

- delivery challans (for supply on approval, supply of liquid gas, job work and other).

What’s the diff between invoice date and due date?

Invoice date refers to the date when the invoice is created on the billbook, while the due date is when the payment is due against the invoice.

How to issue an invoice under reverse charge?

Here, you not issue an invoice different from usual sales or purchase invoices. The only additional requirement is that you need to mention on the invoice that tax is paid on reverse charge.

Is it mandatory to maintain invoice serial number?

Yes, invoice serial number must be maintained strictly.

For example, if invoice is being issued with serial number as INV001, the same format must be maintained. You may change the format by providing a written intimating the GST department officer along with reasons for the same

What all details are required to be mentioned in GSTR-1 for documents issued?

For the following nature of documents issued number of documents prepared, cancelled and net issued along with serial number of each must be mentioned:

- Invoices for outward supply

- Invoices for inward supply from unregistered person

- Revised Invoice

- Debit Note

- Credit Note

- Receipt voucher

- Payment Voucher

- Refund voucher

- Delivery Challan for job work

- Delivery Challan for supply on approval

- Delivery Challan in case of liquid gas

- Delivery Challan in cases other than by way

GST HELPLINE – ACCOUNTING

Under GST all these taxes (excise, VAT, service tax) will get subsumed into one account.

The same trader X has to then maintain the following a/cs (apart from accounts like purchase, sales, stock) –

- Input CGST a/c

- Output CGST a/c

- Input SGST a/c

- Output SGST a/c

- Input IGST a/c

- Output IGST a/c

- Electronic Cash Ledger (to be maintained on Government GST portal to pay GST)

Reduction in raw material cost and other expenses

GST will mean seamless input credits for intrastate and interstate purchases of goods. This will mean reduction in cost of raw materials as input GST can be setoff against the output GST payable on sales. Also GST paid on many services like legal consultation, audit fees, engineering consultation etc. can be setoff against output GST. Currently input credit of service tax paid cannot be adjusted against output excise/VAT.

All this will effectively bring down the expenses.

***Impact on sales may vary depending on the industry and the GST rates.

Accounting principles

GAAP is applicable mandatorily on GST. So, all principles following revenue recognition etc. will be applicable.

Period of retention of accounts

Every registered taxable person must keep and maintain books of account for five years from the due date of filing of Annual Return for the relevant year.

Transition to GST will need to address various aspects of financial reporting systems for proper reporting.

It is important that businesses plan to address changes arising out GST implementation in the best manner to reduce cost of transition and minimize business disruption.

GST CONSULTANTS

States have started scouting for tax consultants to advise them on technical aspects of the goods and services tax (GST) Among other things, the consultants will be required to suggest organisation structure of the department in the GST regime, strategy for transition period and ways to mitigate risks and checklist of tasks that need to be completed before introduction of GST.

Also, the consultant will be required to frame a communication strategy for administration vis-a-vis stakeholders such as industry and traders. Also, the consultant will be imparting training on provisions of the GST Act/Rules and processes to officers of the department.

Besides, the entity will calculate the impact of GST implementation on state revenues keeping in view the present rate of tax in the state and the proposed rate of tax under GST.

/0.png)

/1.png)

/2.png)

/3.png)

/4.png)

/5.png)

/6.png)

/7.png)