Click here to try a return filing tool for free

The laws and procedures for filing GST Returns have focused on interlinking the entire supply chain electronically. Let us now discuss all the monthly, quarterly and annual GST Returns.

What are the categories of registered persons required to file monthly returns under GST?

The following categories of registered persons are required to file monthly returns under GST:

- Non Resident Taxable Person

- Input Service Distributor

- Persons liable for Tax Deduction at Source (TDS)

- Persons liable for Tax Collection at Source (TCS)

- All other Registered Persons

What are the monthly returns required to be filed by persons in category (e) above?

|

Form |

Due Date | Details to be furnished | Form to be filed by |

Additional actions to be taken (if any) |

|

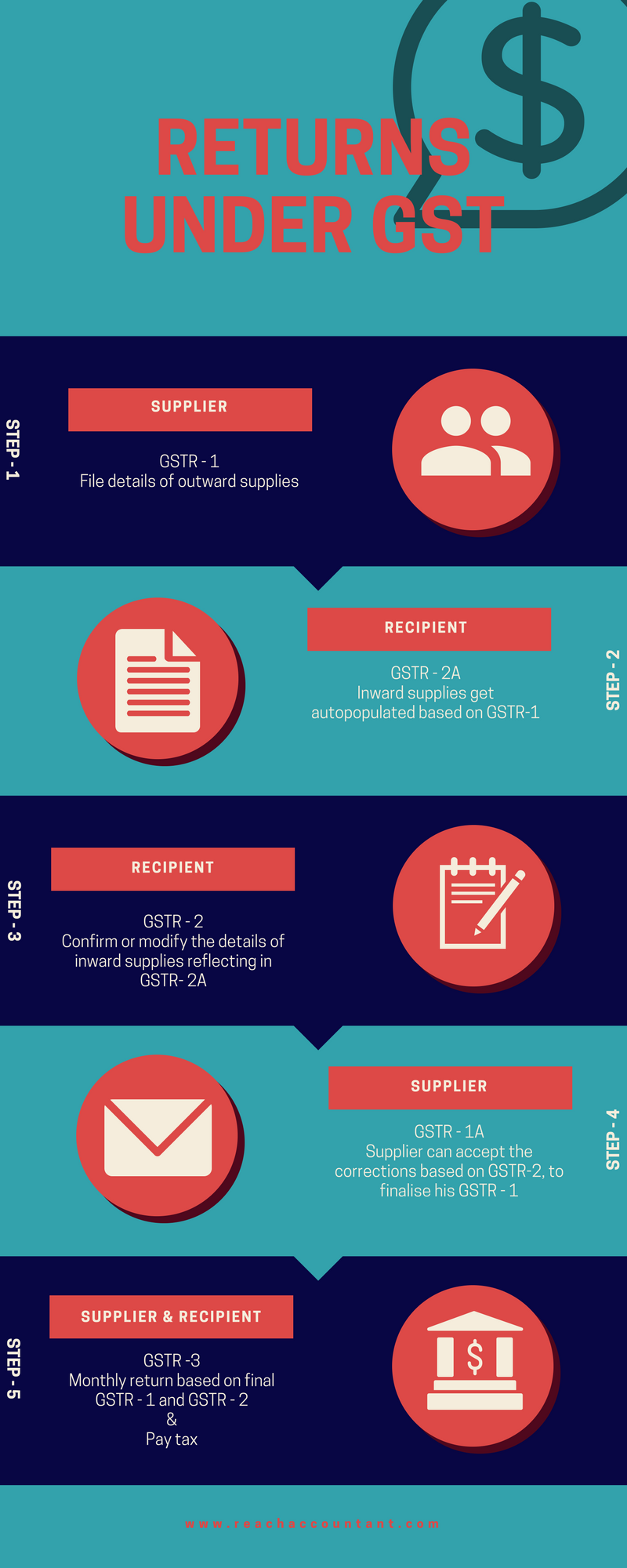

| Step 1 | GSTR – 1 | 10th of succeeding Month | Details of outward supplies of taxable goods or services or both | Registered Supplier | |

| Step 2 | GSTR – 2A

|

Between 11th and 15th of the following month | Details of inward supplies made available to the recipient | Auto-populated on the basis of Form GSTR-1 furnished by the supplier in Step 1 | The recipient should ensure that the inward supplies appearing in his GSTR 2A are matched with his books. Any modification (addition or deletion) in Form GSTR-2A should be submitted in Form GSTR-2 |

| Step 3 | GSTR – 2 | 15th of succeeding Month | Details of inward supplies of taxable goods and/or services claiming input tax credit | Recipient of inward supply | |

| Step 4 | GSTR – 1A | Before 17th of the following month | Details of outward supplies as modified and added by the recipient in Step 2 and Step 3 | Auto-populated on the basis of Form GSTR-2 furnished by the supplier in Step 3 | The supplier should ensure that the outward suplies appearing in his GSTR 1A are matched with his books. Any modification (addition or deletion) in Form GSTR-1A should be submitted in Form GSTR-3 |

| Step 5 | GSTR – 3 | 20th of succeeding Month | Monthly return on the basis of finalization of details of outward supplies and inward supplies along with the payment of amount of tax | Registered persons

|

What are the monthly returns required to be filed by Non Resident Taxable Persons?

|

Form |

Due Date |

Details to be furnished |

| GSTR – 5 | 20th of succeeding Month

or Within 7 days after last day of the period of registration mentioned on his application or 90 days from the date of effective registration (or such extended period of upto 90 days allowed by the proper officer) |

Details of outward supplies and inward supplies of taxable goods or services or both |

The details furnished by the non resident taxable person in GSTR – 5 shall be made available to the receiver of credit in Part A of GSTR 2A.

What are the monthly returns required to be filed by registered person providing Online Information and Database Access and Retrieval (OIDAR) services from a place outside India?

|

Form |

Due Date |

Details to be furnished |

| GSTR – 5A | 20th of succeeding Month

|

Details of outward supplies and inward supplies of taxable goods or services or both |

What are the monthly returns required to be filed by Input Service Distributors?

|

Form |

Due Date |

Details to be furnished |

| GSTR – 6 | 13th of succeeding Month

|

Details of tax invoices on which credit has been received and invoices issued |

The details furnished by the Input Service Distributor in GSTR – 6 shall be made available to the receiver of credit in Part B of GSTR 2A.

Who is liable to deduct tax at source under GST?

The following persons are required to deduct tax at source at 1% from the payment made to the supplier, if the total value of the contract exceeds INR 2,50,000.

- A department or establishment of the Central or State Government

- Local authority

- Government Agencies

No tax shall be deducted at source if the location of the supplier and the place of supply is in a different State or Union Territory from the State or Union Territory in which the recipient is registered.

The above-mentioned deduction of 1% should be on the value of the contract excluding CGST/SGST/UTGST/IGST and cess indicated in the invoice.

Such tax deducted at source shall be paid to the Government through the electronic cash ledger i.e. no input credit can be used to make this payment.

What are the monthly returns required to be filed by Persons liable for Tax Deduction at Source (TDS)?

|

Form |

Due Date |

Details to be furnished |

| GSTR – 7 | 10th of succeeding Month

|

GSTIN of the supplier along with invoices against which the tax has been deducted separately for CGST, SGST and IGST |

The details furnished by the person liable to deduct tax at source in GSTR – 7 shall be made available to the receiver of credit in Part C of GSTR 2A.

The person liable to deduct tax at source shall furnish a certificate mentioning the contract value, rate of deduction, amount deducted and amount paid to the Government in form GSTR – 7A within 5 days from the date of crediting the amount so deducted to the Government.

Who is liable to collect tax at source under GST?

Every electronic commerce operator is required to collect tax at source at 1% on the net value of taxable supplies made through it by other suppliers where the consideration with respect to such supplies is to be collected by the operator.

Net value of taxable supplies = Aggregate value of taxable supplies of goods or services or both by a registered supplier through the operator – Aggregate value of taxable supplies of goods or services or both returned to the registered supplier during the said month.

Such tax collected at source shall be paid to the Government through the electronic cash ledger i.e. no input credit can be used to make this payment.

What are the monthly returns required to be filed by Persons liable for Tax Collection at Source (TCS)?

|

Form |

Due Date |

Details to be furnished |

| GSTR – 8 | 10th of succeeding Month

|

Outward supplies of goods or services or both effected through it, supplies of goods or services or both returned through it and amount of tax collected |

The details furnished by the person liable to collect tax at source in GSTR – 8 shall be made available to the receiver of credit in Part D of GSTR 2A.

What is the late fee payable for delay in filing the monthly returns?

If any registered taxable person who fails to furnish the above details in the respective returns within the due dates, they will be liable to pay a late fee of INR 100 for every day of delay from the said due date to the date of filing subject to a maximum of INR 5,000.

Is revision of monthly returns possible?

There is no provision to revise the returns filed by the taxpayer. However, the taxpayer can rectify the details in the returns of the subsequent tax periods filed by him. The returns formats are having separate tables for inserting the details pertaining to the previous tax periods.

What are the returns required to be filed by Persons who have opted for the Composition Scheme?

Persons registered under the Composition Scheme are required to file quarterly returns. These are explained in detail in my article Composition Scheme Under GST.

What are the annual returns required to be filed by registered persons?

|

Form |

Due Date | Form to be filed by |

Details to be furnished |

| GSTR – 9 | 31st Dec of the following year | Registered Dealer | Consolidated details of all the inward and outward supplies. ITC availed and GST paid |

| GSTR – 9C | 31st Dec of the following year | Registered Dealer having aggregate turnover during the financial year of more than INR 2 crore | Annual accounts audited by a Chartered Accountant or Cost Accountant and reconciliation statement (of the books to the annual returns) to be submitted |

| GSTR – 9B | 31st Dec of the following year | Every e-commerce operator required to collect tax at source | Outward supplies of goods or services or both effected through it including supplies of goods or services or both returned through it, amount of tax collected at source (TCS) |

What is the late fee payable for delay in filing the annual returns?

Any registered taxable person who fails to furnish the annual return, he shall be liable to pay late fees of INR 100/- for every day during which such failure continues subject to maximum of an amount calculated at 0.25% of his turnover in the state.

How are the liabilities and payments of a registered person recorded in the GST portal?

All the liabilities and payments will be recorded in Electronic Ledgers of each taxpayer.

|

Form |

Ledger Name |

Contents |

| GST PMT – 1 | Electronic Tax Liability Register | All liabilities of a taxable person under GST shall be reflected as a debit entry in Electronic Tax Liability Register and on discharge of any liability through electronic credit ledger or electronic cash ledger or reduction in the liability, such amount shall be reflected as a credit in the liability register |

| GST PMT – 2 | Electronic Credit Ledger | Every claim of input tax credit will be available to the credit of the Electronic Credit Ledger |

| GST PMT – 3 | Electronic Cash Ledger | Any amount deposited on account of GST / TDS / TCS shall be credited to Electronic Cash Ledger |

What is the due date for payment of tax under GST?

All taxes due to the Government namely CGST/ SGST/ IGST by the taxpayer other than composite taxpayers is to be paid on a monthly basis by 20th of the succeeding month.

What are the payment modes available under GST?

The deposit of tax to the Government can be made through any of the following modes:

- Internet banking through authorized banks

- Credit card or Debit card after registering the same with the Common Portal through the authorized banks

- NEFT or RTGS from any bank

- Over the Counter (OTC) through authorized banks, for deposits upto INR 10,000 per challan per tax period, by cash, cheque or demand draft

What is the order of discharging the tax liability under GST?

Every person has to discharge his tax liability and other dues in the following order:

- Self-assessed tax and other dues related to returns of the previous tax periods

- Self-assessed tax and other dues related to returns of the current tax period

- Any other liability (eg. Penalty)

What is the consequence for delay in payment of GST?

A registered person shall pay interest at the rate of 18% p.a. for the period for which tax (or part there of) remains unpaid i.e. from the date after the due date upto the date of payment.

No penalty will be leviable if the registered person pays tax and interest there on within 30 days from the due date or in case a show cause notice has been issued, within 30 days from the date of issue of show cause notice.

What is the procedure for payment of GST?

Step 1: File the returns as discussed above.

Step 2: Generate a draft challan by logging into common portal. Basic details of tax payer such as name, address, email, mobile no., GSTIN will be auto populated in the challan.

Step 3: Fill in details such as amount of tax (CGST, SGST, IGST), interest, fees payable. The tax payer can partially fill in the challan form and temporarily “save” the challan for completion at a later stage. A saved challan can be “edited” before finalization.

Step 4: Submit the details and a final challan will be generated. A final challan cannot be modified and will be valid for 15 days. The final challan generated, will have a 14-digit (yymm followed by 10-digits) Unique Common Portal Identification Number (CPIN).

Step 5: Within the validity period of challan, tax payer has to make payment for net tax liability through prescribed modes.

Notifications and Public Announcements to make implementation of GST in businesses more simple

Relaxation in Return filing time-lines for first 2 months

A summary return (single page) form in GSTR-3B will required to be filed on self-declaration basis for first 2 month i.e. July and August by 20th day of next month. i.e. for the month of July, a summary return needs to be filed by 20th August after paying appropriate taxes, and for the month of August, the same needs to filed by 20th September.

However, GSTR-1 with invoice level details needs to be filed for the month of July by 5th September, and for the month of August by 20th September. GSTR-2 and GSTR-3 for these 2 months will be filed thereafter. It means matching for 1st two months of July & August will take place only after 5th/20th September respectively.

Postponement of implementation of provisions relating to TDS and TCS

- The provisions of Tax Deduction at Source and Tax Collection at Source will be brought into force from a date which will be communicated later.

- Persons who will be liable to deduct or collect tax at source will be required to take registration, but the liability to deduct or collect tax will arise from the date the respective sections are brought in force.

- The persons who were liable to be mandatorily registered under GST as they were supplying goods or services through electronic commerce operator who is required to collect tax at source will not be liable to register till the provision of Tax Collection at Source is brought under force unless they are so liable as a result of their aggregate turnover being higher than the threshold limit (INR 20 lakhs/ INR 10 lakhs as the case may be) or any other category of mandatory registrations.

/0.png)

/1.png)

/2.png)

/3.png)

/4.png)

/5.png)

/6.png)

/7.png)

Thumbs up

Thanks for sharing

Great information with good infography

Visit our GST centre at to know all about Tally for GST

Thanks Neha.