Dummies GST Guide – All you need to know about GST in India in less than 60 seconds:

A Complete GST Guide for India to understand the impacts, register or migrate from existing taxes and understand compliances under GST for Businesses.

Goods and Services Tax is a comprehensive tax levied on supply of goods and services across India. GST is expected to be rolled out in 2017 and will replace the current tax systems like excise, VAT, Service Tax etc. GST will unify the tax system across the country and will promote free trade of all items. GST Guide for India explains all the important information which a business in India will have to be aware of.

Table of Content

- Introduction

- Registration

- Invoicing

- Purchases

- Movement of Goods

- Accounting

- Tax Preparation

- Tax Filing

- Compliances

- Assesment

- Refund procedure under GST

- Tools and Software

- Industry wise GST

- Useful Links

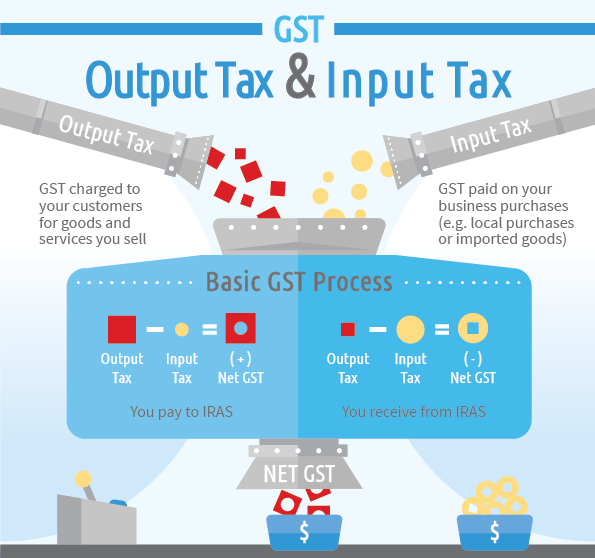

What is GST? How is it better than the current Tax System like VAT, Service Tax, Excise etc

Goods and Services Tax is a comprehensive tax levied on supply of goods and services across India. GST is expected to be rolled out in 2017 and will replace the current tax systems like excise, VAT, Service Tax etc. GST will unify the tax system across the country and will promote free trade of all items.

Two key benefits of GST over existing Tax Systems:

- If you are a manufacturer or trader, currently your input tax can be adjusted on VAT only. Service Tax paid cannot be claimed as an input. However in the unified tax system, you can claim credit for all services, purchases and manufactured goods (as supply replaces service, sale and manufacture as a tax event)

- GST can make compliance easier as it subsumes multiple taxes and makes the point of taxation less ambiguous. Adoption of Cloud Accounting Software like Reach will make it super easy for compliance.

Who should register for GST Number?

The following business will have to register with GST:

- If your turnover is more than 20 Lakhs in a year (10 Lakhs for North-east India), Then you will have to register with GST.

- Business selling inter-state

- Business liable to pay tax under reverse charge

- Agents supplying on behalf of a taxable person

- Input Service Distributor

- Sellers on e-commerce platform

- All e-commerce operators

- Person responsible to deduct TDS

What are the types of GST which will be imposed?

| Nature of Levy | Levyable on | Adjusted against |

| Central GST | Local supply of Goods and Services | CGST and IGST |

| State GST | Local supply of Goods and Services | SGST and IGST |

| Integrated GST | Interstate supply and Imports | Against all |

How does GST affect different businesses?

Please click on the links below to read more about how it affects different business

- GST for e-commerce companies

- GST for Supermarkets

- GST for Manufacturers

- GST for Textile stores

- GST for Jewellery Shops

What are the documents needed for GST Registration?

The following documents are needed for GST Registration:

- PAN Number, Mobile Number and email ID

- Photograph of the owner

- Registration Certificate of the company

- Rental Agreement or Proof of ownership of the place of business

- First page of the Bank Statement

- Authorised signatory approval letter or resolution

How to apply for GST Registration?

- Log on to gst.gov.in

- Fill in Part A of GST REG 01

- Submit along with your PAN, mobile number and email ID

- You will now recieve a One-time password on your phone and email

- Now Fill Part B of the Registration form and attach the documents mentioned above

- Now a Registration Certificate will be issued to you within 3 days.

How to move to GST from VAT?

- If you are registered with Central excise and have a valid PAN, you will automatically be migrated to GST

- A Provisional Certificate of Registration will be issued in GST REG-21

- You have to submit and apply for Registration by submitting REG-20 Form within 6 months

- After submission, you will be issued a Final Registration Certificate in REG-06

How to move to GST from Excise?

- If you are registered with Central excise and have a valid PAN, you will automatically be migrated to GST

- A Provisional Certificate of Registration will be issued in GST REG-21

- You have to submit and apply for Registration by submitting REG-20 Form within 6 months

- After submission, you will be issued a Final Registration Certificate in REG-06

How to move to GST from Service Tax?

- If you are registered with Central excise and have a valid PAN, you will automatically be migrated to GST

- A Provisional Certificate of Registration will be issued in GST REG-21

- You have to submit and apply for Registration by submitting REG-20 Form within 6 months

- After submission, you will be issued a Final Registration Certificate in REG-06

What are the types of Returns to be filed for GST?

For a manufacturer, trader, wholesaler, distributor etc

| Date | Return |

| 10th | GSTR-1 |

| 11th | GSTR-2A |

| 15th | GSTR-2 |

|

20th

|

GSTR-1A |

| GSTR-3 | |

| GST-ITC1 | |

| GSTR-3A | |

| 31st Dec | GSTR-9 |

For a Composite Dealer

| Date | Return |

|

Quarterly

|

GSTR-4A |

| GSTR-4 | |

| Annual | GSTR-9A |

For a Input Service Distributor

| Date | Return |

| 11th | GSTR-6A |

| 13th | GSTR-6A |

For Tax Deducter

| Date | Return |

| 10th | GSTR-7 |

| — | GSTR-7A |

For e-commerce provider

| Date | Return |

| 10th | GSTR-8 |

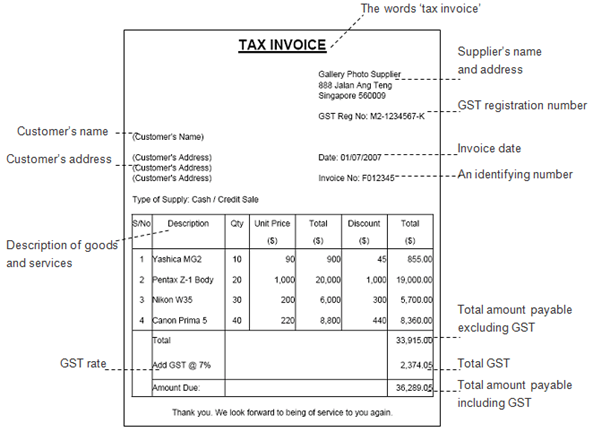

What is the Format of a GST Invoice?

There are two types of GST Invoice you can raise

- Tax Invoice

- Bill of Supply

Rules for the Tax Invoice

- For Goods, The Tax Invoice should be issued at the time of removal of goods or delivery which ever is earlier

- For Services, The Tax Invoice should be issued within 30 days of supply of service

- Three copies of the Tax Invoice should be printed

- One for recipient

- Duplicate for Transporter

- Triplicate for Supplier

- The following details should be displayed in the Tax Invoice

- The Tax Invoice should have unique serial numbers (number or Alpha numeric)

- The State Name and State Code Should be mentioned

- GST Identification Number should be displayed

- HSN Code for the product/ service needs to be mentioned

- Taxable value after deducting discount should be displayed

- The State GST, Central GST and Integrated GST should be shown seperately

- If the supply is meant for export, the following details should also be mentioned

- Supply meant for Export on payment of IGST/ on bond without payment of IGST

- Number and Date of ARE-1 (application for removal for export)

Rules for Supply Invoice

- The Supply Invoice is a consolidated tax invoice and can be raised only for bill value less than Rs. 100/-

- The following details should be mentioned in the Invoice

- The Tax Invoice should have unique serial numbers (number or Alpha numeric)

- Details of the receiver

- GST Identification number

- Value of the Goods

Which is the best GST Software to use for e-commerce companies?

As all the Tax Filings will have to be done electronically, its important to choose your accounting software wisely.

Tally

Tally is the old fashioned legacy software of India. Though its widely used, It has disadvantages of not being on the cloud and compromises security. If you are considering a GST software, It will be wise to move to a Cloud based Accounting System which has the capabilities to manage a e-commerce company

Reach Accountant

Reach is the only Online Accounting Software with GST Capabilities and ability to give you features specific to supermarkets. It can further sync transactions directly from your front-end website like Shopify, Kartrocket or Magento. Alternatively, you can also sync your website to our backend using a free Rest API. To get a quick demo of our product, you can Visit www.reachaccountant.com

What is a debit note and what is the format of a Debit Note under GST?

Debit Note is raise if there is a subsequent increase in the value of the GST Invoice raised.

The debit note should include the following details:

- It should prominently be displayed as Revised Invoice or Supplementary Invoice

- Name, Address and GST Identification Number

- The note should be numbered consecutively with a date

- If the recipient is unregistered, then the state code

- Serial number and the date of the original Tax Invoice

- Taxable value of the increase or reversal

- Signature or Digital Signature

What is a Credit note and what is the format of a Debit Note under GST?

Credit Note is issued if there is a sales return or a reduction of Invoice value.

The debit note should include the following details:

- It should prominently be displayed as Revised Invoice or Supplementary Invoice

- Name, Address and GST Identification Number

- The note should be numbered consecutively with a date

- If the recipient is unregistered, then the state code

- Serial number and the date of the original Tax Invoice

- Taxable value of the increase or reversal

- Signature or Digital Signature

How to transfer the input credit on my closing stock to GST?

Yes. You can transfer the input credit from your CENVAT or VAT held on your closing stock if the following conditions are satisfied:

- The closing stock should be held in the form of Raw materials, Work-in-progress or Finished Goods and intended to be used in taxable supplies

- The benefit of the credit should be passed on in the way of reduced prices to the recepient

- You should be eligible to claim input tax credit under GST

- You should have proof of Invoices or tax paying documents for the current credit and these documents should be less than 12 months old

How to file GST Returns

The procedure to file a GST return is different from the current practice.

Here is how you file a GST Return:

- You will have to file the returns electronically in the GST portal.

- Before 10th of every month – All companies will have to file their details of Sales (Supplies) in GSTR – 1

- From 11th to 15th of every month – You purchase details along with inputs will be auto-populated

- You can check them and do any corrections in Form GSTR-2

- The proposed corrections can be accepted/ rejected by the supplier

- On 20th of every month the auto-populated GSTR-3 will be available for submission along with the payment

- You can pay and submit the return

- Acknowledgement will be provided in GST-ITC1

How to make my GST Compliance easy?

As all the Tax Filings will have to be done electronically, its important to choose your accounting software wisely. Reach is the only Online Accounting Software with GST Capabilities and ability to give you features specific to your business. To get a quick demo of our product, you can Visit www.reachaccountant.com

Is it possible to get refunds of Input Credit?

Refunds will be available in following cases:

- Excess payment of tax due to a mistake or inadvertence

- Export (including deemed export) of goods/services. No exemption on inputs/input services will be provided and the same will be required to be claimed as a refund.

- Finalisation of provisional assessment

- Refund of pre-deposit, including refund arising in pursuance of an appellate authority”™s order

- Payment of duty/tax during investigation but less liability arises at the time of finalisation of investigation/ adjudication

- Refund of tax payment on purchases made by UN bodies, supplies to canteen stores department (CSD) canteens, paramilitary forces canteens, etc.

- Tax credit on inputs used for manufacturing/generation/ production/creation of tax-free supplies or non-GST supplies

- Refund of carry-forward input tax credit: ITC accumulated due to inverted duty structure will be refunded.

- Refund on account of year-end or volume-based incentives provided by the supplier through credit notes: Application to be filed along with certification and input tax credit at the buyer”™s end and output liability at the supplier”™s end to get reduced simultaneously; important for e-commerce entities for year-end as well as volume discounts

- Tax refund for international tourists

The following key points have been mentioned for the refund process:

- Focus of the refund process is to grant refunds with the least possible submission of documents and ensure easy process

- Refund application to be submitted online in the prescribed format within one year from the prescribed relevant date along with other supporting documents

- CA certificate required if re

fund exceeds specified limit (in other cases, self-certification will be sufficient)

fund exceeds specified limit (in other cases, self-certification will be sufficient) - Option to file refund application either on the GSTN portal or through respective state/central tax portals

- Preliminary scrutiny of refund applications to be carried out within 30 working days

- Refund to be paid by the government electronically through NEFT/RTGS/ECS

- For refund in excess of specified amounts, pre-audit of refund application has to be carried out

- Recommended rates of interest: For delayed payment of refund @ 6% and for default in payment of GST @ 18%

- Interest on refund to be payable from the last date when refund should have been sanctioned

- GST law may provide for adjustments of refund claims with outstanding tax demands

/0.png)

/1.png)

/2.png)

/3.png)

/4.png)

/5.png)

/6.png)

/7.png)

{kind=link}

If service is provided and invoice also issued before 30th June, but bill is pending as on 30th June…can the service recipient claim input tax credit under transitional provision?

You shared excellent information on about calculating the tax returns of a successful business easily by using online system software , I read this post and remember the best points especially ” customer service management ” mentioned in this article which help me for running a business successfully with the help of professional accounting .If you want to start a business successfully then you must read this article carefully and keep it in your mind all the best points of a great article which help you to running a business successfully with the professional accountant .

Thanks

Please Flow tin number gst ingormation give please Call 9873240355

Please Flow tin number gst ingormation give please Call 9873240355